[ad_1]

Each week, Cut the Crap Investing founder Dale Roberts shares financial headlines and offers context for Canadian investors.

Scotiabank says 8 rate hikes are on the way

Scotiabank’s Derek Holt shared that we could see eight rate hikes in Canada over the next two years. That is aggressive. Rate hikes would likely deflate the real estate market and perhaps stock market and, by design, put a brake on personal spending and on economic activity.

Increased borrowing costs can mean less money available for consumption.

From the Financial Post article:

“Policymakers led by Governor Tiff Macklem will begin a series of eight 25-basis-point hikes in July of next year, Scotiabank’s Derek Holt said Wednesday on BNN Bloomberg Television. That will be followed by moves in September, October, and December. Holt predicted the the pace of tightening would then slow, with quarterly moves in 2023 bringing the policy rate to 2.25% by the end of that year.”

Of course, central banks will use the rate-hike weapon to battle inflation; and those inflation worries are gathering steam. The Bank of Canada signalled that it will put an end to the bond buying program known as quantitative easing.

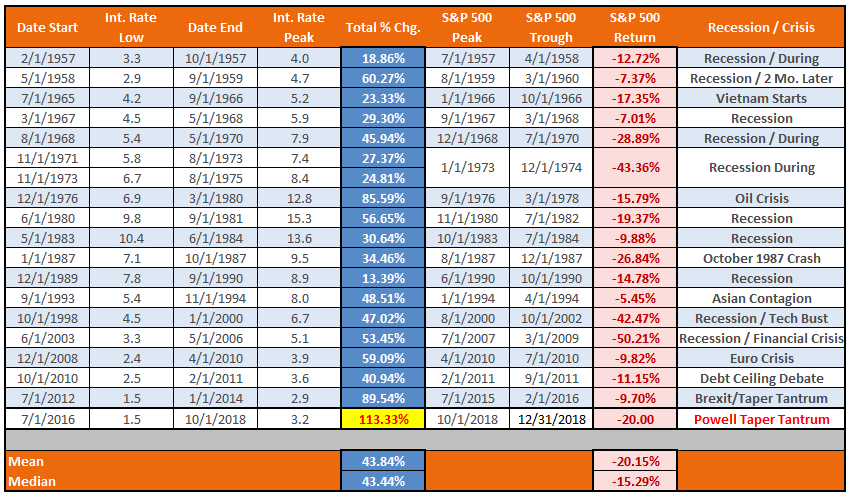

Previously we looked at that tapering and what a taper tantrum is. We do know that historically, an aggressive increase in rates usually will lead to stock market corrections and recessions. Here’s the go-to chart on that event, courtesy of Lance Roberts, Chief Strategist RIA Advisors.

Of course, no one knows that will happen with rates and bond yields or the stock markets in the near term. The key is to be aware and prepared.

We should always be prepared for corrections—that is, be emotionally prepared. And the portfolio should be balanced to be able to temper the volatility and protect your wealth, as well, if you are in retirement or are nearing retiring.

That can mean holding those out of favour bonds, as I wrote last week. In fact, Roberts suggested—in an email exchange and in counter-intuitive fashion—the time to buy longer-term treasuries is when we see those first rate hikes. If those do kill the economy and end the stock-market party, it will be bonds time to shine—again.

I would not favour any market timing. I already have core bond funds, short-term bond funds and longer-date treasuries in my portfolios. I’ll be happy to hold my nose and add some more over the next few months or year.

It’s called portfolio rebalancing.

Many investors favour those shorter-dated bonds, as they will usually fall in price less than longer-dated bonds in a period of rising rates. And those shorter-dated bond funds will also more quickly add the higher yields that are available in the market—as bonds in the fund mature and are replaced.

There’s nothing wrong with holding core bond funds you find in core couch potato portfolios. However, core bond funds will come under pressure in a rising rate environment.

I asked Martin Pelletier, portfolio manager at Wellington-Altus Private Counsel, for his opinion on the potential of rising rates and the messaging from The Bank of Canada. Read this from our email exchange:

“I think it was a prudent move from the Bank of Canada, as it could slow down an overheated housing market causing already over-levered households to reconsider additional real estate speculation. It also sends a clear message to the federal government that it’s soon time for them to be accountable for their balance sheet.”

And, Pelletier also pointed to the risk for that conservative, and traditional, 60/40 portfolio.

“Rising rates will also have a negative impact on those conservative investors in fixed-income investments. This also creates the same problem for the traditional 60/40 investor.”

I like how Horizons did a re-think of the traditional balanced portfolio. They ramped up the equity exposure slightly (10%) and added some other assets.

Given these times, Pelletier will alter the fixed-income strategy and assets for clients. He added:

“For example, we now have the lowest bond weighting allowed in our client portfolios and are replacing with equity-linked, custom-built notes that have yields above inflation rates and built-in downside barriers. We have been reducing other interest-rate sensitive investments like the tech-heavy S&P 500 and reallocating to global value.”

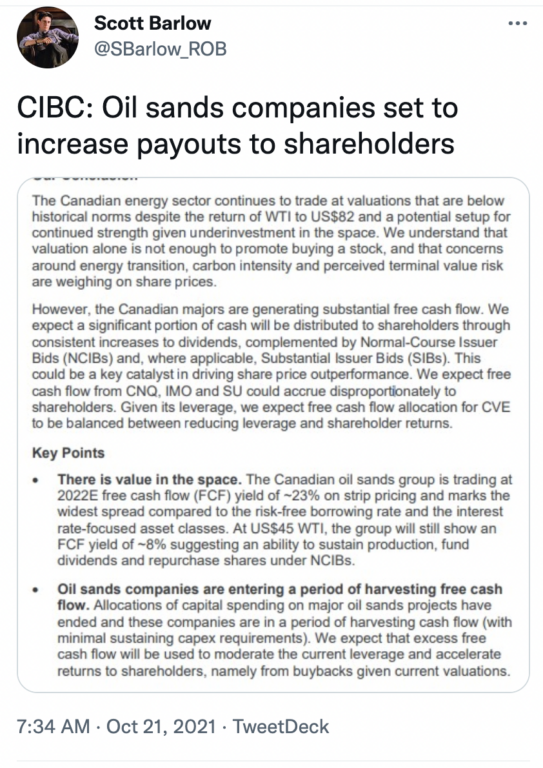

The incredible value and potential in oil and gas sector

The energy story just won’t go away, and many investors (and drivers) have had just about enough pain at the pumps. On the other side of the coin (or other side of the pumps) energy investors are raking it in. And there is a loud chorus suggesting that the profits will continue to flow for oil and gas energy producers.

Not advice, but I had put energy producers on the table for investors over a year ago. That’s also about 140% ago (positive total returns) as well over the last year, using the TSX Capped Energy Index as a benchmark.

Look no further than the recent returns from energy producers.

Out-of-favour Suncor (SU) reported this week and the free cash flow was more than impressive. While it missed estimates, Suncor delivered revenue of $10.21 billion, an increase of 58% year over year. From its quarterly report and by way of Seeking Alpha.

The company recorded operating earnings of $1.043 billion ($0.71 per common share) in the third quarter of 2021, compared to an operating loss of $338 million ($0.22 per common share) in the prior year quarter. The company had net earnings of $877 million ($0.59 per common share) in the third quarter of 2021, compared to a net loss of $12 million ($0.01 per common share) in the prior year quarter.

With ample free cash flow they were able to retire debt at a good clip. The shareholder return is more than impressive.

In the third quarter of 2021, the company returned $1.0 billion to its shareholders, through $704 million in share repurchases and payment of $309 million of dividends, and it reduced net debt by $2.0 billion.

Suncor recently doubled and restored its dividend to 2019 levels after a dividend cut. The share price increased 9% on the open after reporting on October 28. The stock closed up over 13% for the day.

No sector is expected to generate greater free cash flow, if current oil price levels are maintained or move higher.

Thanks to Scott Barlow of the Globe and Mail for this tweet.

The market is starting to take notice, offers this tweet from Liz Ann Sonders of Charles Schwab. Oil stocks vs S&P 500:

Also, on the same front, we’re seeing commodities outperform stocks in 2021. Of course, it’s not either/or, but the use of commodities as a portfolio and lifestyle hedge.

There is always risk with any asset or asset class. In this post, Eric Nuttall, portfolio manager at Ninepoint Partners, addresses the risks of oil and gas investing. Some of the risks include COVID-19 resurgence, the U.S. shale producers ramping up again and OPEC members turning on the taps.

That is a great read, and Eric offers a measured but certainly pro-investment stance. The title of that post is “The oil party has just begun.”

Personally, I’m more than happy to have invited myself to the party. To invest or not, is certainly a personal decision.

Some market history, just for fun

No one knows with any certainty how the stock markets will perform in any given period. But there are some seasonal trends in play. November and December are typically strong months for stocks, especially when October is positive.

The following chart is month-to-date, to October 26.

Source: S&P Global

The following note is courtesy of DataTrek received via email.

“With October rapidly drawing to a close, today we have an update on our seasonal U.S. equity return and volatility analyses to see what they signal for the S&P 500’s performance in November and December. In our last review at the end of September, we showed, that since 1980, on average, October (+1.1 pct) not only recoups September’s typical losses (-0.6 pct) but also adds to the year’s gains.

“So what can history tell us about S&P returns during the balance of 2021?

“#1: The S&P usually rallies in November and December. Since 1980, the S&P 500 has been higher nearly three-quarters (73 pct) of the time in the last two months of the year, and up an average of +3.3 pct overall. When the S&P is higher in November and December, it’s gained an average of 5.6 pct compared to a loss of 3.1 pct during years with a negative return for those two months.

“#2: Positive momentum in October helps drive better returns during the remainder of the year. For example, the S&P has only rallied +5 pct in October in eight years or a fifth of the time since 1980. During those years, the S&P was up 8.0 pct on average in October. In the following November and December, the S&P was up an average of 3.8 pct and advanced nearly two-thirds of the time (63 pct, slightly lower than in point #1 but not statistically significant).

“This momentum also works in the other direction: the S&P has only been down by 5 pct or more three times in October since 1980, but also fell in November and December in each of those years (down an average of 4.7 pct across the 2 months).”

There are investors that partake in this kind of market timing, but that’s certainly not the norm, and it’s not for me. I would not hold back monies to take advantage of excess monthly gains that might arrive in November and December.

Though it is interesting to see that the trend observed by DataTrek did play out last year as well, with November and December of 2020 delivering generous returns.

I will report back in the new year to check if November and December of 2021 added to this positive seasonal trend.

Once again, just for fun.

A look at big tech earnings in the U.S. and Canada

There was a mix of nervousness and high expectations leading into the reporting season for the monster U.S. tech stocks. We’ll also look at Canadian tech darling Shopify (SHOP).

Perhaps no company has profited more from, and during, the pandemic than Amazon (AMZN). The pandemic created conditions for the work-from-home, stay-at-home and shop-from-home economy. But their fortunate positioning has hit a few snags.

Amazon reported on Thursday, October 28, and it signalled it will need to navigate through the maze of labor supply shortages, increased wage costs, global supply chain issues and increased freight and shipping costs.

On October 22, we discussed how labour shortages have messed with supply chain issues, and how that mix might pose a challenge for many companies. Amazon is now on the receiving end of that unique economic blend.

The e-commerce giant reported third quarter revenue was up 15% to $110.8B. Operating income decreased to $4.9B in the quarter from $6.2B a year ago.

That said, the market shrugged it off, and the stock was up over 1.5% on Thursday, after recovering from a weak open. The stock has had an incredible run, up almost 1,500% over the last 10 years and 343% over the last five.

Source: Seeking Alpha

It is a very expensive stock after its pandemic run and has mostly been catching its breath over the last year.

And Apple falls

I hold Apple (AAPL) and, while I would never trade around earnings, I watch and read the reports with great interest. Apple is also a victim of those supply chain issues and states that demand is not a problem for the company.

Apple shares fell as much as 5% in after-hours trading Thursday as the company reported fourth-quarter sales that rose from a year ago, but fell short of Wall Street analysts’ expectations.

Revenue increased by almost 29% to $83.36B year over year but, again, it missed analysts’ expectations for the quarter. Or, as I like to say: The company didn’t miss it, the analysts did.

From Seeking Alpha.

We see that Apple has become a much more diversified company over the last several years, with revenue and profits from many streams.

• Products revenue of US$65.08 billion vs $68.72 billion consensus,

• iPhone revenue of $38.87 billion vs $41.60 billion consensus,

• Mac revenue of $9.18 billion vs $9.31billion consensus,

• iPad revenue of $8.25 billion vs $7.16 billion consensus,

• Wearables, home and accessories of $8.79 billion vs $9.28 billion consensus,

• And service revenue of $18.27 billion vs $17.57 billion consensus.

What a beast!

The stock has had a good run. And while not quite as expensive as Amazon, it may need to rest a while. But only time will tell.

Source: Seeking Alpha

Growth is great no matter, depending on where you might be in the wealth building process. For retirees, you’ll see that the yield is very small. You’ll have to slice off some very small pieces to make your own homemade Apple dividends (sell shares). Having owned the stock since 2014, I have created those dividends on a couple of occasions to help fund trips.

Some really juicy dividends and capital appreciation is a wonderful tag team for the retiree.

If you hold a core index-based portfolio you’ll have ample exposure to Apple and Amazon and other big tech. And when you sell shares in an index ETF you are essentially creating your own homemade dividend. Your profits will be a mix of dividends and share appreciation.

Source: BlackRock / S&P 500 (IVV)

Microsoft (MSFT) and Apple continue to battle it out for the title of the most valuable stock on the planet. Thanks to cloud earnings Microsoft had a wonderful quarter.

Source: Seeking Alpha

The markets applauded that earnings report. As a shareholder, I put my hands together as well.

Alphabet (GOOG), the parent company for Google, delivered with beats on the revenue and earnings front. Just check out these numbers.

Source: Seeking Alpha

Facebook (FB) has its own reputational issues and has decided to undergo a rebranding.

Facebook is now Meta.

To my eye that is a fitting and scary Tweet, just in time for Halloween.

The Canadian tech darling

Shopify (SHOP) investors said “ka-ching, ka-ching” as the Canadian tech darling (and most valuable publicly-traded Canadian company) rang up some impressive numbers.

The share rose on a 46% increase in revenue year over year. That could be called Canada’s Amazon.

It’s where they keep the growth

The tech sector is quite vulnerable to inflation risks. And the words overvalued and expensive get thrown around with regularity when describing U.S. tech stocks and by extension U.S. stock market. This is certainly where they keep the growth.

Regular readers know that I also hold the opinion that U.S. tech is very expensive. On the plus side, the earnings growth is helping to make it less expensive.

Once again, taking ridiculous tech profits and redistributing to risk-off assets or more defensive stocks can help reduce that risk.

It’s called rebalancing.

Dale Roberts is a proponent of low-fee investing and he blogs at cutthecrapinvesting.com. Find him on Twitter @67Dodge.

The post Making sense of the markets this week, October 31, 2021 appeared first on MoneySense.

[ad_2]

Source link