[ad_1]

Kyle Prevost, editor of Million Dollar Journey and founder of the Canadian Financial Summit, shares financial headlines and offers context for Canadian investors.

Deflating expectations

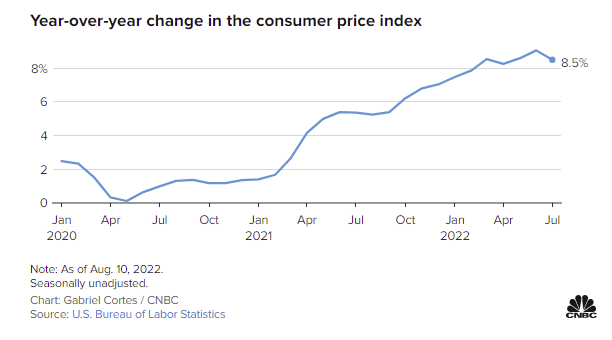

Because valuations of the world’s assets are so heavily dependent these days on the inflation numbers and accompanying interest rate moves, investors eagerly awaited this week’s Consumer Price Index (CPI) report in the U.S.

When news broke that we might be past “peak inflation,” the markets rallied and are now not far off from where they were a year ago—even if they have more to do to achieve previous highs. While news of an 8.5% year-over-year increase in the CPI would have been considered shocking at any point in the past few decades, it represented a decline from 9.1% last month, and was lower than the 8.7% predicted by economists. “Core CPI” (the consumer price index figure after food and gasoline are stripped from the equation) rose 5.9%, which was also comforting news for inflation hawks.

Some notable takeaways from the report include:

- Energy prices declined 4.6% (including 7.7% for gasoline)

- Food prices increased by 1.1%

- Shelter costs increased by .5% (and are up 5.7% over the last year)

- Electricity increased 1.6%

- Used vehicles declined in price by .4%

- Airline fares fell by 1.8% (and are down nearly 8% from a year ago)

- Wages increased by .5% on a “real” (after inflation) basis

When you combine these disinflationary numbers with the decreasing inflation expectations of consumers released by the New York Fed survey on Monday, it all adds up to the fact that the tightening monetary policy enacted by central banks around the world appears to be working.

The reason that inflation expectations are such a big deal is that inflation can be a self-fulfilling prophecy. When people expect costs to go up, they demand higher wages, then businesses start to raise prices faster in order to keep pace with increased costs, and the spiral begins.

Consequently, when survey respondents indicated that they expected inflation to average “only” 6.2% over the next year, and 3.2% for the next three years, experts are hoping it stops the inflationary spiral in its tracks.

As these inflationary pressures begin to abate, most observers expect the central banks around the world to slow down the pace of interest rate increases. Of course, once we get more certainty with the interest rate, it will be easier to reach stable equilibriums on the valuations of companies and long-term bond pricing. This sentiment was likely the main catalyst for broad market movement this week.

Tough to beat the master and the mouse

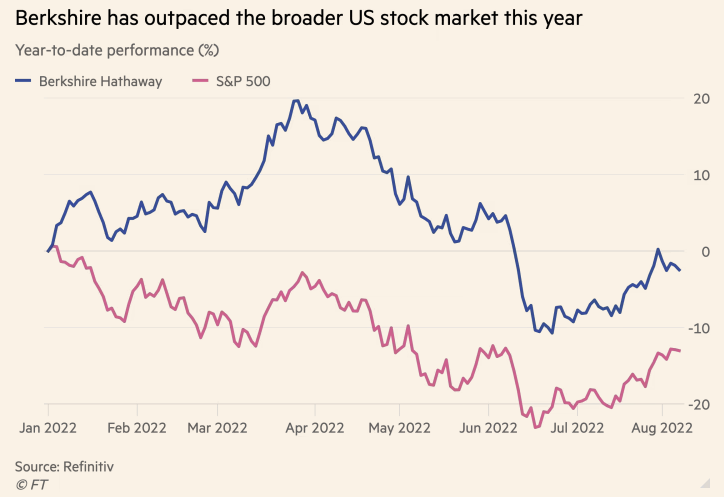

Warren Buffett revealed that he continued to be greedy as others were fearful, as the Berkshire Hathaway (BRK.B/NYSE) quarterly report stated that the Oracle of Omaha deployed another USD$6.2 billion of the Berkshire war chest, as well as rewarding shareholders with USD$1 billion in share buy-backs. (All figures in this article are in U.S. currency, unless otherwise stated.)

However, it’s worth noting that while $6.2 billion is a decent chunk of change for any company, it still represents a less greedy Buffett than in the first Quarter, when Buffett really put Berkshire’s cash to good use by purchasing shares worth $51.1 billion. Purchases included: Citigroup, Paramount Global, Ally Financial, Chevron, Occidental Petroleum, HP and Activision Blizzard.

While the fact that Berkshire booked a $53-billion loss from the depreciation of shares within its broad portfolio of companies got most of the attention, Berkshire was quick to point out that its operating income (how its underlying companies actually did, as opposed to simple stock pricing) rose by 39% year over year to $9.3 billion.

While Berkshire’s stock hasn’t exactly set fire this year, the company’s value investing-based approach held up pretty well relative to the rest of the S&P 500.

In terms of broad takeaways, the slowdown in Buffett’s spending slightly concerns me. Given that Berkshire still has more than $100 billion in cash on its balance sheet, I would’ve hoped it would be more confident in finding more opportunities to make excellent long-term investments. Clearly, the mixed economic picture is affecting investors’ decision making at this point.

Meanwhile, Disney’s (DIS/NYSE) earnings report last Wednesday was all positive. Earnings per share came in at $1.09 (versus a predicted $0.96), while both revenues and the all-important Disney+ subscriptions came in well ahead of analyst expectations as well. With the surge in post-lockdowns “revenge travel,” it’s no mystery why the parks, experiences and products divisions saw revenues increase 72% year over year. Disney shares rose 6% as investors processed the upbeat news.

Canadian investors looking to get portfolio exposure to Disney and Berkshire can do so through CDRs on the Neo exchange.

Bausch suffers from IBS—that’s Irritable Balance Sheet

Because Canada’s healthcare sector is so small comparatively speaking, when one of our few large companies sees a year-to-date drawdown of more than 80%, it’s pretty big news.

The massive hit was due to a court decision involving Bausch’s (BHC/TSX) patent for the drug Xifaxan. This drug is used to treat irritable bowel syndrome (IBS), and because Bausch was set to have exclusive rights of production until 2029, substantial profit margins were baked into the company’s current valuation.

When the court decision awarded Norwich Pharmaceuticals the right to produce a generic version of the drug sooner than expected, Bausch investors saw those rewarding profit margins evaporate. Bausch quickly stated that it would be contesting the decision.

Current quarterly results didn’t exactly inspire confidence either, with revenues down from last year, and an overall loss of USD$145 million. While Bausch is headquartered in Laval, Quebec, it is listed on both the TSX and NYSE, so it chooses to report financial results in USD.

Many Canadians might be more familiar with the company’s former name of Valeant. Valeant was briefly Canada’s largest company by market capitalization, before suffering a well-publicized collapse. While Bausch was able to jettison the Valeant name, the company is still encumbered by USD$22 billion in debt on its balance sheet.

We recently wrote about Canadian Healthcare Stocks on Million Dollar Journey, and our skepticism on Bausch was quickly proven to be well founded.

In other Canadian earnings news, Canadian Tire (CTC/TSX) saw its profits decrease 30% year over year to CAD$2.45 per share. Management cited the impact of exiting the Russian market as a drag on both revenues and profits. While profits were down, revenues did increase by 12.4% from the year prior. Investors weren’t enthused with the news, as the stock was down 4.6% on Thursday.

Mining investors strike gold

While I’m not a huge fan of investing in commodities due to their volatile nature, plus the lack of valuation metrics available, Canada’s mining companies are another matter. For example, while I have no idea whether the price of gold is going to go up or down, I do know that if gold consistently stays around $1,800 per ounce, gold mining companies can continue to make quite a lot of money.

Regardless of gold’s relationship to Bitcoin, or its status as an “inflation-fighter,” I know that large gold mining companies make money if the price stays above $1,200.

Canada’s big gold miners all recently reported very healthy earnings seasons.

Barrick Gold (ABX/TSX): Adjusted earnings per share came in at CAD$0.24 (versus a predicted CAD$0.23), while total revenue was down slightly from a year ago. The company noted strong results across its major properties, but like nearly every other company in the world these days, faced cost pressures to its bottom line.

Franco Nevada (FNV/TSX): Posted adjusted earnings per share of CAD$1.02 (versus a predicted CAD$0.96) and slightly higher revenues than last year.

Agnico Eagle Mines (AEM/TSX): Had a strong quarter as well, beating earnings estimates with an earnings per share of CAD$0.76 (versus a predicted CAD$0.73). Revenues were up substantially last year as well.

Canadian investors looking to get direct or indirect exposure to gold have a variety of options.

ETFs, like the Horizons Gold ETF (HUG/TSX), track the price of gold through futures contracts, while the iShares S&P/TSX Global Gold Index ETF (XGD/TSX) is an index of the largest gold companies in the world. (Barrick is roughly 15% of the index, Franco Nevada 13%, and Agnico Eagle 10%, while Newmont Gold from Colorado garners about an 18% share of the index currently.) Finally, the iShares Gold Bullion ETF (CGL/TSX) allows investors to semi-directly hold physical gold bullion.

I’ve written a more in-depth description about each of these Canadian gold investment options over at Million Dollar Journey.

While all that glitters is not profitable, the markets liked what they saw this week.

Kyle Prevost is a financial educator, author and speaker. When he’s not on a basketball court or in a boxing ring trying to recapture his youth, you can find him helping Canadians with their finances over at MillionDollarJourney.com and the Canadian Financial Summit.

The post Making sense of the markets this week: August 14 appeared first on MoneySense.

[ad_2]

Source link