[ad_1]

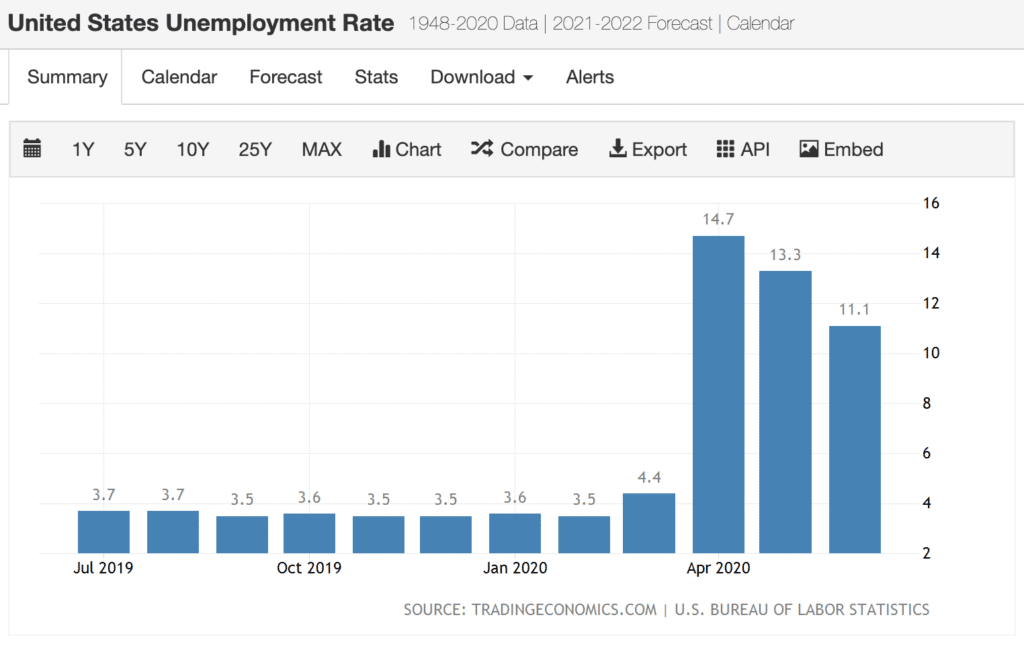

Do you remember all those soothing economic numbers that were floating around as recently as February? You know – the record low unemployment rate of 3.5%, and the record high stock market, with the Dow Jones Industrial Average closing at almost 30,000?

It seems like ages ago, doesn’t it?

The coronavirus happened and changed it all – in just three months. The stock market fell by a third before recovering somewhat in April, while unemployment exploded. It reached 14.7% by the end of April, with Goldman Sachs predicting it may go as high as 25% – a level not seen since the Great Depression.

(Source: Trading Economics from data supplied by the U.S. Bureau of Labor Statistics)

Since economic downturns are actually really normal events, the best strategy is to build financial resilience. There’s nothing we can do to stop a crisis from happening, but we can and should get our own financial houses in order to minimize the impact.

The following 7 strategies will help you do just that.

1. Take Any Financial Shocks Off the Table

One of the factors that characterizes economic downturns is financial shocks. One of the best ways to build financial resilience is to prepare for them.

Start by reviewing your insurance policies. If need be, increase the amount of car insurance you have. It should be enough to protect your assets if you’re involved in an accident that’s determined to be your fault. If you do have adequate coverage, get some auto insurance quotes to see if you can lower your premiums.

This is also an excellent time to purchase a private life insurance policy. If you’ve been relying on life insurance from your employer, that may go away if you lose your job. Check out options for low cost life insurance and get a policy today.

And in case of an emergency, you may need a line of credit that can be accessed on short notice. Check with your bank or credit union to see if you can get an unsecured line of credit. Alternatively, you can apply for a personal loan, or even a low interest credit card.

You won’t want to access any lines of credit now, since staying out of debt may be critical to your financial wellbeing. But you’ll want to have open lines of credit available when an emergency hits. Lenders have already started tightening up restrictions for making lines available a few months from now.

2. Cut Costs Wherever You Can

Since income often becomes uncertain during economic downturns, cutting costs is one of the best ways to be prepared in advance.

I’ve come up with 85 ways you can save money in your own household budget. By selecting and implementing just a few you may be able to cut hundreds of dollars out of your budget.

And speaking of budgets, you should have one if you don’t already. Millions of people function without budgets, at least until an economic downturn hits. But sometimes all you need is the right budgeting software to get you moving in the right direction.

Budgeting will show you exactly where your money is going and help you identify which expenses you can cut or eliminate. That will not only reduce your expenses, but it’ll also make extra money available to pay down debt or build up savings.

3. Pay Down Debt Ahead of Time

One of the biggest expenses in many household budgets are debt payments. Whether it’s car loans, student loans, or credit cards, debt payments can take a big chunk out of your budget. If that’s true, begin to pay down debt now and work toward paying off as much as you can.

You may need to implement some aggressive debt payoff strategies. If so, that’s best done sooner than later. If you lose your job, any payment you can eliminate or reduce will improve your resilience.

If you have student loans, look into refinancing them while you’re still employed. Shop around for lenders that specialize in student loan refinances. Since these loans are often large, refinancing them has the potential to get you large savings from a lower payment.

If you have credit card debt, take advantage of 0% introductory APR offers with balance transfer credit cards. Getting a break on interest for 12 to 18 months can help you pay down your credit card balances a lot faster, since the payments you would allocate toward interest can be made toward principal.

4. Pad Your Emergency Fund

One of the very best ways to build financial resilience into your life is by loading up your emergency fund. Even if you already have one in place, now is an excellent time to begin increasing the balance.

During economic expansions, having between one- and three-month’s living expenses in your emergency fund may be sufficient. But in an economic downturn, you may need to expand that to six months or longer.

Sure, you may get unemployment benefits if you lose your job. But that probably won’t come close to replacing your current income. Just as important, emergencies have a way of popping up during times of economic turbulence. The more money you have sitting in your emergency fund, the better you’ll be able to weather it all.

If you’ve got your emergency fund sitting in a local bank or credit union, you’re probably earning interest of something only just above zero. You can and should fix that problem.

There are high-yield online savings accounts paying interest rates as high as 2%. That may not sound like a lot of money, but it’s more than 20 times the 0.06% being paid at average banks and credit unions. You owe it to yourself to earn as much interest on your emergency savings as you can get.

5. Establish an Advanced Savings Strategy

While an emergency fund will protect you against short-term expenses and income disruptions, now is also an outstanding time to begin building savings for longer-term needs.

One such need could be a run of unemployment that exceeds the amount of money you have in your emergency fund. By having a second-tier level of savings, you’ll have funds available if your emergency fund is exhausted.

You may also want to begin building savings for goals like paying off your car loan or having extra money available to cover the out-of-pocket costs not covered by your health insurance plan. Still another possibility is that you may need to start a business if you lose your job and find yourself unable to get a new one.

For medium term savings goals, you’ll want to put your money where it’ll be just out of immediate reach (so you won’t grab it for short-term needs), but where you’ll also earn even higher returns.

You can do that by investing in peer-to-peer lending platforms, like LendingClub. There you’ll have an opportunity to earn double-digit returns on your investment, with relatively low risk. Investigate other ways you can earn high interest on short-term investments so you’ll have funds available for whatever the future may hold.

6. Invest in Yourself

Most people don’t think of investing in themselves as an investment. But when you consider that your income is probably your single biggest asset, it’s one of the very best investments you can make.

The most obvious way to invest in yourself is to improve or acquire any skills or certifications that may help you in your job or your career. You may be one skill or one credential short of your next promotion. And even if you aren’t promoted, that skill or credential could be the one that lands you your next job.

You may also want to consider acquiring any skills you need to create a second income (more on that in the next section), or even in preparation for the launch your own business.

You can often take courses at local community colleges to acquire very specific skills. And some certifications require only the completion of a correspondence or online program to earn. The results can add thousands of dollars per year to your income – and just as important – make you more valuable to your employer. That will matter because during an economic downturn the people who are laid off first are the ones with the least value to the employer. By improving your skill set and qualifications, you’ll make yourself much less expendable.

There are also plenty of ways to invest in yourself that can help you make additional money outside your job. Think about what it is you would like to do, or what you have an interest in, and begin studying ways to earn money from it. Sometimes just acquiring a single skill will enable you to convert a hobby into an income source.

Speaking of which…

7. Build a Passive Income Stream or Side Hustle

One of the very best ways to build financial resilience for an economic downturn – or even during good times – is by creating additional sources of income.

One of the very best sources of additional income can be had by building passive income streams. There are actually dozens of ways to create passive income, it’s just a matter of choosing the one that’ll work best for you. For example, I’ve managed to create seven different income sources, some of which are passive. The great thing about passive income streams is that they give you the ability to earn money while you’re busy doing other things.

Still another option, and one you should definitely consider, is creating a side hustle. Not only will this generate an additional source of revenue that will add resilience to your finances, but it could represent the beginning of what will eventually become a full-time business if you lose your primary job.

One of the best ways to build a side hustle is by making money online. I’m doing that with this blog, but there are plenty of other ways you can make it happen. You owe it to yourself to investigate the opportunities. One of the big advantages of making money online is that you won’t have any geographic restrictions. If you have to relocate, maybe to take another job, your online business will come with you.

Don’t be intimidated by the idea of creating a side hustle. According to a recent article on Fortune, nearly half of Americans under 35 currently have a side hustle. You could be one of them – all it takes is an idea and a commitment.

The Bottom Line

No one knows exactly how the coronavirus recession will play out. But that’s the case with every economic downturn we’ve ever had. Recessions can’t be avoided, and neither can the financial dislocation they bring. But by building financial resilience into your life, you can minimize and even eliminate the worst a recession can throw at you.

Reevaluate every area of your finances – your insurance coverage, expenses, savings, and income – and look for ways to improve each.

Even if you think it’s too late for you to prepare for this recession, now is an excellent time to get ready for the next one. After all, it’s already on your mind, so you have all the motivation you’ll need.

And don’t underestimate your ability to protect yourself during this recession. The worst course of action is inaction. You may not be able to get your finances exactly where they need to be right now, but you may surprise yourself at how much you can improve your situation in just a few months. That will matter too, because it’s likely we’ll still be in this recession even then.

It’s never too late – or too early – to build financial resilience in an economic downturn. Today isn’t too soon to get started.

The post How to Build Financial Resilience in An Economic Downturn appeared first on Good Financial Cents®.

[ad_2]

Source link