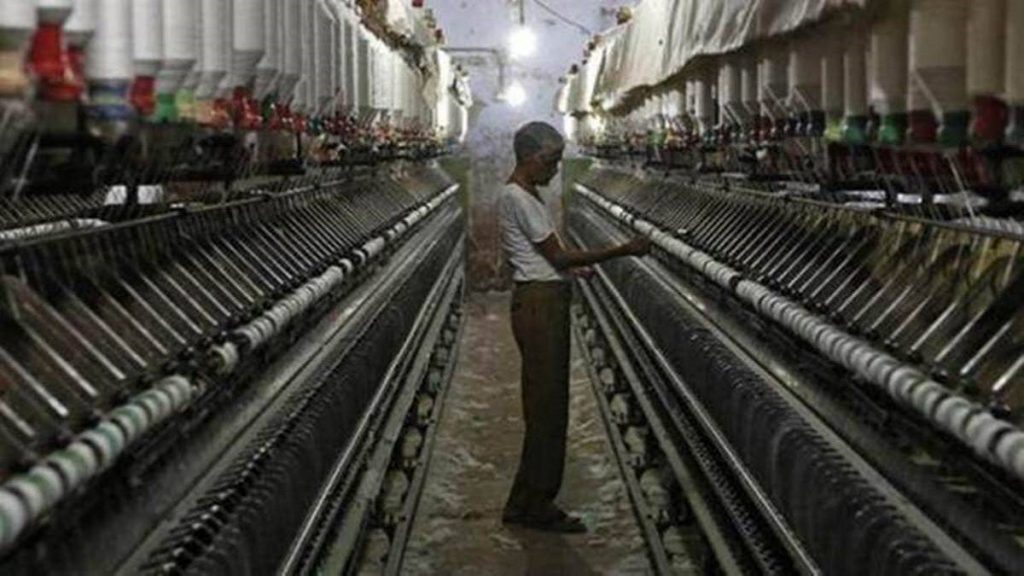

[ad_1] In May 2020, finance minister Nirmala Sitharman raised the thresholds for the tags of micro, small and medium enterprises (MSMEs), acknowledging that the earlier definitions were creating an unintended incentive for units to remain ‘small’. She cited pan-India data of MSMEs scaling up, but for hundreds of units in South Delhi’s Okhla Industrial Area (OIA), the journey since then has been decidedly downhill. The pandemic and a relentless rise in labour and input costs have crippled most units here. So, one could find several units in this chaotic industrial town in the national capital, which in 2020 fit the criteria for a ‘medium’ enterprise announced by the minister, but have since been relegated to the ‘small firm’ category, as their turnovers slid steeply from over Rs 100 crore then to Rs 40-50 crore or less now. And many ‘micro’ units have since shut operations or come to have only a minimal, sombre existence. Large sections of the factories here – mostly manufacturers of garments, leather, pharmaceuticals and packaging materials – are also facing an acute labour shortage as not all of the migrant labourers who left the city during the pandemic have returned. While MSMEs in other parts of the country may also be facing similar problems, Okhla units also have the additional constraints of being housed in the national capital, where environmental norms are now being diligently enforced. Also, implementation of minimum wage norms have inflated labour costs. In his early 40s, Mahipal makes ready-made garments for kids in a small factory at Sanjay Colony in phase-II of OIA. From 10 people in the pre-pandemic days, his employee strength has now come down to just three and even they are not getting adequate work due to lack of demand from wholesalers. As a result, his monthly sales are down 70% now from the pre-pandemic levels. “If things go on like this, we will have to bring down the shutters in a not-so-distant future,” he says in exasperation. Operating from the same area among 250-odd other wholesale traders is Vishal Chowdhury, who deals in dupattas. His sales have more than halved compared with the pre-pandemic days. “The cost of the raw materials has gone up by around 50%. Only a portion of the extra cost can be passed on to the retailers,” Chowdhury says. The recent cotton shortage also hit his business, as his regular suppliers have cut operations. Not surprisingly, at the the garment hub in OIA, only a couple of trucks were waiting for uploading goods on Friday. Since the lockdown, only 3-4 trucks operate in the industrial area compared with 12-13 earlier, a labourer says. A ‘green tax’ – Rs 1,700-1,800 for a 14 ft diesel truck – has dented the margins of truckers. A couple of kilometres away, Deepak Gupta is finding it difficult to run his printing unit at full capacity. Gupta does not face any demand shortage, but the cost of his key raw material – art paper – has risen from Rs 60/kg a year ago to Rs 115/ kg now. Labour costs have gone up too. “Stringent pollution checks are making the business all the more difficult to run,” he says. Not surprisingly, many printing units are leaving Okhla to settle in nearby Noida, Gurgaon and Faridabad. OIA includes a cluster of 600 printing units with annual turnovers between Rs 5 crore to Rs 50 crore. More than 20 have closed down and around 40 units have shifted to Noida and Faridabad. Even among the operating units, most are using barely 50% of the capacity. Just a week ago, one firm sold a costly imported machine and it is now left with only one, Gupta informs. “The buyer of the machine will soon start operating from outside Delhi,” he says. “Labour is a big problem. While we pay a worker the minimum wage of around Rs 16,500 a month, he will work for just Rs 9,000-9,500 in Noida or Faridabad. Our margins are getting squeezed. Printing press business in Okhla will survive for a maximum of five more years,” Gupta predicts. Garment exporters from OIA had been doing relatively well till the pandemic hit in 2020 thanks to regular buyers in Europe. They are now busy finding new buyers in other shipments to Europe have become erratic after the pandemic. “In the absence of the Europe market, we are targeting the US market. Apart from leather garments that we used to deal with earlier, we have now added cotton garments to our basket,” says Lallan Kumar, who works as a manager in one of the many export firms in the area. Okhla Chamber of Industries president Arun Popli says OIA has now turned into a hub of micro enterprises. Higher electricity costs, costlier labour and exorbitant parking fees have led many factory owners to vacate their places and rent them out to new tenants who are turning them into offices, he adds. “All the big units of Okhla have fled to various parts of NCR primarily because of higher labour costs. Okhla started losing its charm from 2016-17 when the Delhi government increased minimum wages. The wages here are now double the level in neghouring areas,” Popli says. Not many Okhla units have benefitted from the government’s flagship guaranteed loan scheme, the coverage of which was widened by Rs 50,000 crore to Rs 5 trillion in the latest Budget, or the Credit Guarantee Trust for Micro and Small Enterprises. These schemes were extended by the Narendra Modi government, ackowledging the need for a protracted period of succour to start-ups and small businesses as they grappled with fallout of Covid-19. [ad_2] Source link