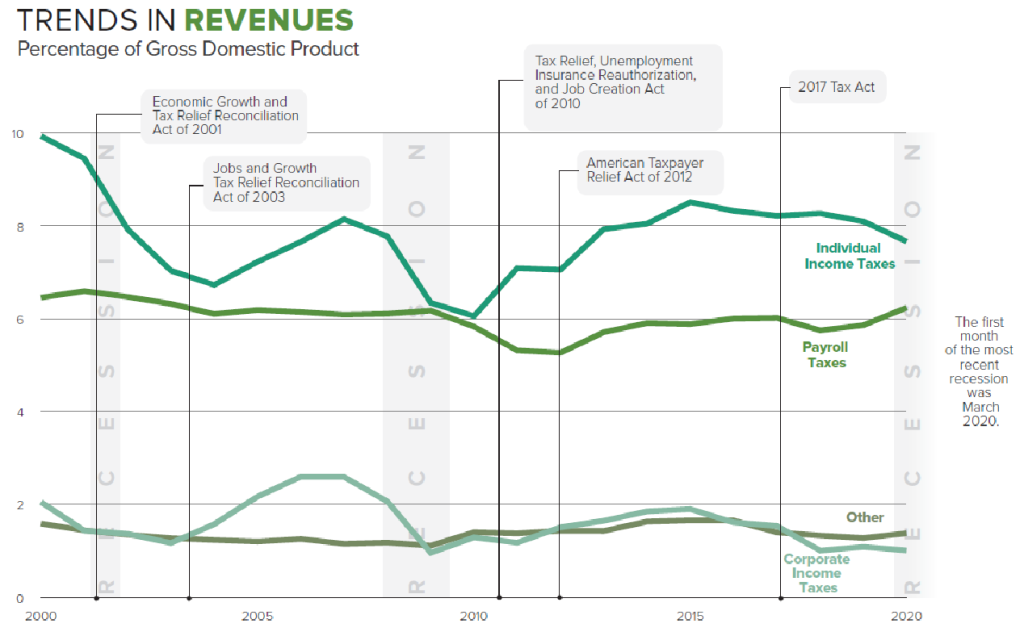

[ad_1] “Our new Constitution is now established, and has an appearance that promises permanency; but in this world nothing can be said to be certain, except death and taxes.” — Benjamin Franklin, in a letter to Jean-Baptiste Le Roy, 1789. Thankfully, after more than a year with innumerable challenges, it appears that the pandemic will end. From an economic perspective, the government acted boldly to support households and businesses through the crisis with monetary and fiscal stimulus. Now, just as the recovery has commenced, after a four-year pause we are at the beginnings of another tax debate. In this column, my aim is to provide you with some of the context for this debate with respect to the state of the U.S. federal budget, particularly on the revenue side, and of overviews of the 2017 Tax Cuts and Jobs Act (TCJA) and President Biden’s tax plans and the two 2021 proposals: The American Jobs Plan and The American Families Plan. Government budget and tax statistics For those looking to quickly understand the current state of the U.S. federal budget, I would recommend looking at the new set of infographics put together by the Congressional Budget Office (CBO). As shown there, in fiscal year 2020, the federal government spent $6.6 trillion, while it took in $3.4 trillion in revenue. I expect I will be writing more about the implications of budget deficits that exceed $3 trillion in future columns, but today I wanted to focus on the revenue side. In FY 2020, the infographic shows that of those $3.4 trillion in revenues, individual income taxes accounted for $1.61 trillion, payroll taxes for $1.31 trillion, corporate taxes for $212 billion, and other revenues for $289 billion. Other revenues include remittances from the Federal Reserve ($82 billion), excise taxes ($87 billion), customs duties ($69 billion), estate and gift taxes ($18 billion), and miscellaneous fees and fines ($35 billion). I highlight these data both because it is interesting to see the relative magnitudes of these different revenue sources, and because it might surprise some people, given the amount of ink spilled on some of the smaller items. Next, it is worth looking at how tax revenues have changed over time. In Exhibit 1, revenues are measured here by the CBO as a share of GDP. The economy grows over time, and revenues on a dollar basis grow with it. Measuring these revenues as a share of GDP scales them appropriately. Tax revenues tend to increase when the economy is booming and fall during recessions. In addition to these changes, the different revenue components can rise or fall if tax policy changes. The major tax bills, including the TJCA, are shown in this chart. These four types of revenues are ranked the same as they are in dollar terms; and in total, revenues were 16.3% of GDP in FY 2020. On average, that share has been 16.8% over the last 20 years. In FY 2020, both individual and corporate taxes declined as a share of GDP due to the recession. Exhibit 1, Source: CBO Goals of tax reforms Understanding some of the top-line numbers with respect to the federal government’s revenues, let’s review the TJCA and discuss the changes that Biden’s tax plans are proposing. It is helpful to begin by thinking about what each proposal aimed to accomplish. At the highest level, tax reforms can be placed in one of three categories: tax increases, tax cuts, or revenue-neutral “fundamental” tax reforms. The goals of the first two are straightforward – to raise more revenue to address rising deficits or offset additional spending, in the first case, or to boost the economy by cutting taxes, in the second. A fundamental tax reform attempts to improve the efficiency with which taxes are collected to improve the economy’s functioning. Clearly, actual proposals can be combinations of these categories and the labels can sometimes be in the eye of the beholder. For the two proposals discussed here, the TCJA was a fundamental tax reform/tax cut with a goal to increase the rate of growth, while the Biden administration proposals overall represent a tax increase motivated to support increased spending. To its proponents, the TCJA was a fundamental tax reform with goals to lower marginal tax rates and broaden the tax base by eliminating deductions and exemptions. There were also efforts to simplify the tax code by doubling the standard deduction, which greatly reduced the number of households that needed to itemize deductions. Proponents forecast that this type of tax reform would make U.S. corporations more competitive, would increase productivity and economic growth, and as a result, would lead to a revenue neutral outcome – even though households and businesses would be paying at lower marginal rates. Those opposed to these changes argued that the cut in marginal rates for corporations and individuals would lead to a disproportionate tax break for those with higher incomes. That concern highlights another common goal of tax reforms, i.e., to alter the distribution of taxes paid. Again, it is helpful to look at the data on this question. Exhibit 2 below shows the income before taxes, means-tested transfers, income taxes, and after-tax income by household income quintile. A few items to note: The highest income group has much higher average income on both a pre-tax and after-tax basis. This group also pays a large share of federal taxes. (Looking within this highest 20% of earners, this pattern is also true when you look at the top 1% or top 0.1%. The tax code is progressive, with higher earners paying at a higher rate). The middle three quintiles pay a smaller share of federal taxes, but don’t receive much in the way of means-tested transfers. As a result, their level and share of after-tax income is similar to that for their pre-tax income. The lowest 20% of earners receive most of the means-tested transfers and pay no federal income taxes. (They do pay payroll taxes). The combination means that after-tax income is higher than pre-tax