Twitter to sell mobile ad unit MoPub for $1 billion

[ad_1] Twitter to sell mobile ad unit MoPub for $1 billion [ad_2] Source link

Twitter to sell mobile ad unit MoPub for $1 billion Read More »

[ad_1] Twitter to sell mobile ad unit MoPub for $1 billion [ad_2] Source link

Twitter to sell mobile ad unit MoPub for $1 billion Read More »

[ad_1] A wireless home camera that installs in minutes, delivers good quality video and is packed with features typically found in pricier models [ad_2] Source link

Godrej Spotlight PT Home Camera Range: Watch over your loved ones from afar Read More »

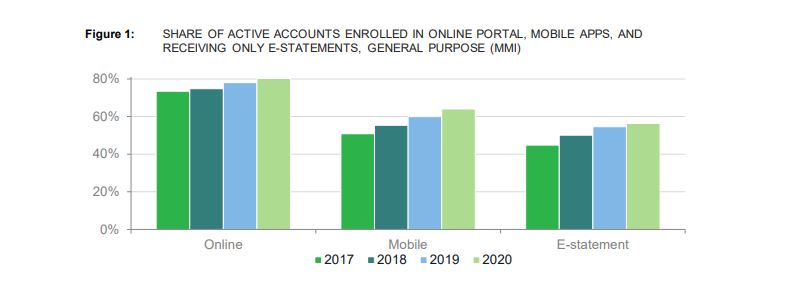

[ad_1] The Consumer Financial Protection Bureau’s (CFPB) fifth biennial report to Congress on the consumer credit card market was released last week, highlighting an upwards trend in adoption of financial technology. The CFPB found digital engagement – whether reflected in enrollment in online portals, enrollment in mobile apps, opt-in rates to e-statements over paper equivalents or electronic payment of credit card bills – is growing consistently across all age groups and on nearly every platform type. According to the report, the most consumers ever recorded are paying their credit card bills online or via mobile app. Concurrently, the use of paper-based payments has declined. The share of consumers enrolled in automatic payments also continued to increase in 2020, with 20% percent of active accounts surveyed enrolled in automatic payments at year-end compared to 16% in 2018. Consumers who are using this automatic payment option reported the elimination of late fees as the number one reason to choose automation. The CFPB pointed to the pandemic as the most likely motive for this upwards trend in digital adoption as credit card issuers were faced with a series of challenges in how to address demand for credit, the need for relief and the servicing of existing accounts. “COVID-19 necessitated a sharp adjustment in the operational posture of major credit cardissuers,” the CFPB said. “In some ways, the consumer impact of the acute destabilization in issuer customer service might have been worse if issuers had not established digital servicing channels prior to the pandemic.” The Adoption of Digital Photo courtesy of CFPB According to the report, pandemic-driven concerns around the use of cash or touching a payment terminal appeared to further the digital evolution at the point of sale, driving enablement and adoption of contactless payment methods such as “tap and pay” and digital wallets. Concerns over contact coupled with bank branch closures, shortened hours, postal service delays or social distancing may have also incentivized consumers to use online or mobile tools to check balances or cash a check more frequently than in pre-pandemic periods. To assist with pandemic-driven longer wait times, the CFPB also reported a spike in AI-powered chatbots and user engagement with these bots. Also noteworthy is the rise in the share of accounts enrolled in mobile apps, which has more than doubled in only five years, from 30% in 2015 to 64% in 2020. Although this adoption is more common in younger consumers, 2020 saw an increase in older generations downloading and utilizing mobile financial tools – a trend the Bureau expects to continue. Innovations the Bureau is Watching As part of the report, the CFPB releases a number of trends in financial innovation that it has either acutely observed or in some cases directly facilitated. In general, the recent additions fell in to three categories: Credit access and availability, particularly for less creditworthy borrowers Fixed-payment features and non-card ‘buy-now-pay-later’ point-of-sale credit products Other innovations, including virtual cards and new forms of rewards redemption Tapping in to credit A number of recent options have become apparent for “credit invisible” borrowers to both acquire credit cards as well as repair their current credit history. The report used Varo Bank as an example as the fintech introduced a credit card which reserves the amount spent from a linked bank account to ensure users never miss a payment. The bureau also pointed to Chime‘s secured credit card, which offers a variable spending limit based on the amount the consumer places in its account, and Self, which offers a secured credit card toborrowers of its credit builder installment loan who allocate a portion of their loan funds to their account without requiring a credit check. Other offerings from Synchrony, TomoCredit, Acima and Apple’s ‘Apple Card Family’ that would allow partners and families to build a shared credit history were also mentioned. BNPL’s boom Since the Bureau’s 2019 report which found some of the buy now, pay later frenzy was already beginning, the CFPB noted market observation that estimate U.S. BNPL lending jumped from $3 billion in 2019 to $39 billion in 2020, and will exceed $100 billion annually within three years. “The extent to which BNPL competes directly with credit cards – either as a means of paymentfor consumers’ purchases or as a means of purchase financing – is unclear,” the CFPB said. For the Bureau, key differences between BNPL loans and credit cards may present risks to consumers as BNPL lenders are not required to consider ability to repay before extending credit. As a result, the bureau reported traditional credit card issuers are investing in more ways to offer their own “fixed-payment”features, possibly in response to BNPL’s explosive growth. Nevertheless, the Bureau acknowledged its success and integration in industry leaders like Affirm, Klarna and Afterpay, as well as its prosperity overseas. The post CFPB report finds spike in digital adoption of financial services during pandemic appeared first on HousingWire. [ad_2] Source link

CFPB report finds spike in digital adoption of financial services during pandemic Read More »

[ad_1] Imagine having a beloved dog or cat who becomes gravely ill only to find out the care they require will cost thousands of dollars. This scenario is heartbreaking but also incredibly common. Even worse, many pet owners don’t have the funds to foot the bill. How much can healthcare for pets set you back? According to CareCredit, a healthcare financing company, treating a dog or cat with cancer costs pet owners $4,000 on average, whereas the cost of removing a foreign object from a pet’s stomach can cost $2,955 to $3,262. What if your pet breaks a bone? Repairing the injury and providing rehabilitative care for a cat costs around $2,257, and the same care costs $2,371 for a dog. It’s no wonder many pet owners purchase pet insurance, a financial product meant to defray the costs of caring for your pet. Like health insurance, pet insurance requires a monthly or annual premium as well as a deductible before you can use it. However, having pet insurance can mean forking over a few hundred dollars (vs. thousands of dollars) if your pet becomes ill or injured. How Pet Insurance Works According to the Insurance Information Institute (III), pet health insurance works similarly to health insurance for humans. These policies cost money, and they can come with deductibles, co-pays and caps on coverage. While pet insurance is most commonly purchased for cats and dogs, individuals can also purchase pet insurance for exotic birds, potbelly pigs, rabbits and other animal companions they cherish. Like health insurance for people, the cost of pet insurance varies based on an array of factors. The Insurance Information Institute (III) says pet insurance costs are tailored to individual animals based on: Age of the pet Overall health Level of coverage you choose Type of animal you’re purchasing coverage for Generally speaking, older animals require pricier pet health insurance premiums, and some pet insurance companies have an age limit. With Healthy Paws Pet Insurance, for example, you can only buy coverage for animals up to the age of 13. Also note that pre-existing conditions are rarely covered by pet insurance, and that some breeds of dogs or cats may be more difficult to insure. If you have a pet that is especially vulnerable to costly hereditary conditions, for example, you may be limited in the number of pet insurance companies you can use. Types of Pet Insurance As you begin comparing pet insurance companies and policies, you’ll also notice different levels of care. While some companies offer more tiers of coverage, pet insurance policies typically fall into one of three levels: Basic Pet Insurance: This level of coverage is the least expensive option and is meant to stave off catastrophic pet care bills for accidental injuries and serious illnesses. In some cases, basic pet insurance plans only cover injuries caused by accidents. Deductibles tend to be a lot higher with basic pet insurance plans, and caps on coverage limit how much they’ll pay out in a year or over your pet’s lifetime. Comprehensive Pet Insurance: This level of pet insurance coverage costs more in general, but it includes more types of injuries or illnesses as well as office visits, certain types of tests and prescription drugs. Deductibles tend to be lower than you’ll find with basic pet insurance plans, yet caps on coverage still limit how much your policy pays out for animal care. Well Care Pet Insurance: The top tier of pet insurance includes the most robust coverage for pets money can buy. This coverage even includes well care and preventative care, such as flea and heartworm pills and regular vaccinations. These plans tend to come with no deductible or a lower deductible than you’ll get with other pet insurance plans. As you begin shopping around for pet insurance, you should strive to compare quotes from a few different companies. However, you should also have a general idea of the level of coverage you can benefit most from. You will be asked to pay higher premiums in general for a comprehensive plan, including plans with well care visits. However, those higher premiums can afford you higher caps on coverage and more included benefits. Likewise, you can purchase a basic pet insurance plan for a lot less if you’re fine with lower coverage limits and fewer included perks. What Does Pet Insurance Cover? Another detail to note with pet insurance policies is the fact they often exclude certain types of care, as well as injuries or illnesses. Since different pet insurance companies exclude different conditions, this is another area you’ll want to explore before you settle on a pet insurance plan. With that being said, most pet insurance plans cover conditions such as: Illnesses Accidents Some hereditary conditions Some congenital conditions Cancer Diagnostic treatments Hospitalization Emergency care What do pet insurance plans not cover? For the most part, pet insurance plans do not cover pre-existing conditions of any kind. Most pet insurance plans do not offer coverage for routine care and wellness either, and most exclude office visits and exam fees. You’ll also find pet insurance plans that cover accidents only, but this is only true among the most basic plans offered. Average Cost of Pet Insurance How much is pet insurance for dogs? How much is pet insurance for a cat? These are important questions, yet the answer won’t be the same for every pet. As we mentioned already, pet insurance premiums vary widely depending on the animal you want to buy coverage for, their age and their health. The level of coverage you select also plays a role in how much pet insurance costs, as well as the company you buy coverage with. With that being said, the North American Pet Health Insurance Association (NAPHIA) shows the following average pet insurance premiums for cats and dogs in 2020. Accident Coverage Only, United States (2020) Accident and Illness Coverage, United States (2020) Dogs $18.17 per month $49.51 per month Cats $11.13 per month $28.48 per

How Much is Pet Insurance? Read More »

[ad_1] These Custom Growth Charts are so cute! Jane has these Custom Growth Chart Canvas & Wood Frame for just $29.99 shipped right now! This canvas chart is professionally printed on thick durable canvas and comes with a solid oak hanging frame and faux-leather cord. Makes a great gift idea! Psst! We love Jane! Looking for other great Jane deals? Check out our custom Jane page for more of our hand-picked favorite deals each day! [ad_2] Source link

Custom Growth Chart Canvas & Wood Frame only $29.99 shipped! Read More »

[ad_1] Auto output dives in Brazil, Mexico as chip shortages bite [ad_2] Source link

Auto output dives in Brazil, Mexico as chip shortages bite Read More »

[ad_1] This indigenous aircraft is an amalgamation of latest concepts and technologies like relaxed static-stability, advanced glass cockpit, integrated digital avionics systems, fly-by-wire flight control and advanced composite materials for the airframe. [ad_2] Source link

LCA could be a good option for Argentine Air Force, says a source Read More »

[ad_1] Looking for a frugal gift idea? Send someone a FREE 6-pack of Cheryl’s Gourmet Cookies! Right now, Cheryl’s Cookies has their 6-Pack Cookie Samplers for just $9.99 shipped! Plus, these come with a $10 reward card making this basically free! These samplers include six Buttercream Frosted Cookies. Choose from four options. This would make a great frugal gift idea! Thanks, Kosher On A Budget! [ad_2] Source link

Free 6-pack Cheryl’s Gourmet Cookies Gift Sampler after Gift Card {Frugal Gift Idea!} Read More »

[ad_1] Creators of molecule-building precision tools win Chemistry Nobel [ad_2] Source link

Creators of molecule-building precision tools win Chemistry Nobel Read More »

[ad_1] The ambulance will serve 41 villages within a 10 km radius of Kotagiri. This remote region, with a population of 33,570, belongs to the tribal communities like the Badaga, Kotas, Todas, etc. [ad_2] Source link