Biden, Putin set for crucial call over Ukraine

[ad_1] Biden, Putin set for crucial call over Ukraine [ad_2] Source link

Biden, Putin set for crucial call over Ukraine Read More »

[ad_1] Biden, Putin set for crucial call over Ukraine [ad_2] Source link

Biden, Putin set for crucial call over Ukraine Read More »

[ad_1] Winter Session of Parliament 2021 Live News: Kiren Rijiju will table a bill to amend the High Court Judges (Salaries and Conditions of Service) Act, 1954 and the Supreme Court Judges (Salaries and Conditions of Service) Act, 1958. [ad_2] Source link

[ad_1] A San Rafael, California real estate appraiser is being sued for allegedly undervaluing a home by almost 50% because the homeowners are Black. Sausalito, California homeowners Tenisha Tate-Austin and Paul Austin, along with Fair Housing Advocates of Northern California, filed a lawsuit in federal court Thursday alleging race discrimination against Janette C. Miller of Miller & Perotti Real Estate Appraisal and AMC Links LLC, an appraisal management company headquartered in Lehi, Utah. Messages left with Miller and AMC Links on Monday were not returned. The lawsuit is the latest instance of Black homeowners stating that an appraiser has, because of conscious or subconscious racism, thought less of their home’s value, and that no one intervened to overrule the appraiser’s prejudice. By many appraisers own admission, their profession is old and white, and faced with a growing number of race discrimination complaints, though the extent of these complaints is unclear. According to the lawsuit, Tate-Austin, and her husband Austin bought a house in Marin County for $550,000 in 2016. Over the next four years, the couple completely remodeled the home, and later added an accessory dwelling unit. They refinanced their mortgage in 2018 and 2019, and sought to do so again in 2020. It was in this third iteration of mortgage refinancing where the alleged appraisal bias occurred. Miller who, according to her LinkedIn, has operated Miller & Perotti appraisal services since 1992, valued the home at $992,000. The Austin’s claim Miller was lowballing them because of their race. In response, the Austin’s brought in a new appraiser, who the complaint does not identify, and “white-washed” their house prior to the appraisal. “They packed away their family photos, which depicted the house’s occupants as an African American family,” the complaint reads. “They also removed and stored any art that was African or African American themed and stored it where it would not be visible.” Moreover, the Austin’s had a white friend pose as the property’s owner. This friend, “placed some of her own family photos, depicting her white family” around the house “prior to the inspection.” The new appraiser valued the home at $1.482 million – 49% more than Miller’s valuation. Besides the evidence drawn from the second appraisal, the Austin’s claim that Miller was biased because of the sales comparisons she used in valuing the home. Miller’s comparisons included homes in nearby Marin City, the complaint states, that were not like the Austin’s home but may have been selected because Marin City has a higher Black population relative to the rest of Marin County. The complaint does not delve into why AMC Links is also being sued besides a sentence stating that the firm failed to review Miller’s valuation to ensure that it met the Appraisal Foundation’s published standards and was not influenced by race. Appraisal management companies such as AMC Links typically play matchmaker between mortgage lender and appraiser. Federal regulators have envisioned appraisal management companies as a firewall between appraiser and lender. Fair Housing of Northern California also names itself as a plaintiff, contending that their investigation into the Austin appraisal, “diverted resources, including staff time and financial resources, from other investigations and activities.” In July, Fair Housing of Northern California filed a complaint with the U.S. Department of Housing and Urban Development on behalf of Cora Robinson, who alleged racial bias against Class Valuation, an appraisal management company, and Thomas Kearney, an individual appraiser. In addition to officially filed complaints, the Washington Post, New York Times and other widely read publications have anecdotally reported on racial bias in appraisals. However, it is unclear how rampant bias complaints are. For one, the Department of Housing and Urban Development has repeatedly declined to disclose to HousingWire the number of appraiser bias complaints it has received. In a November interview, Melody Taylor, executive director of HUD’s Property Appraisal and Valuation Equity task force, stated that, “Due to confidentiality filings, HUD does not disclose the complaints we receive.” HUD has also told HousingWire it does not disclose investigations that are still pending. In addition to HUD and a few private lawsuits, the Consumer Finance Protection Bureau also receives complaints about appraisers. That federal agency has received 14 such complaints since 2019, though CFPB does not categorize such alleged misconduct as specifically regarding race discrimination. Georgia Kromrei contributed reporting The post California couple sues appraiser for race discrimination appeared first on HousingWire. [ad_2] Source link

California couple sues appraiser for race discrimination Read More »

[ad_1] This 52-Week Gratitude Journals are so cute and perfect to keep you reminded of all the blessings in your life right now! Trying to cultivate more gratitude? Jane has these 52-Week Gratitude Journals for just $9.99 shipped right now! Choose from over 15 styles. This gratitude journal includes questions quotes and prompts throughout the journal and comes with 165 stickers. A perfect gift idea, too! Psst! We love Jane! Looking for other great Jane deals? Check out our custom Jane page for more of our hand-picked favorite deals each day! [ad_2] Source link

52-Week Gratitude Journal only $9.99 shipped! Read More »

[ad_1] Mixing Pfizer, AstraZ COVID-19 shots with Moderna gives better immune response – UK study [ad_2] Source link

[ad_1] People close to the development told FE that Power Grid Southern Interconnector Transmission System project, and the Nagapattinam Madhugiri Transmission line are the two major assets that are likely to be transferred to PGInvIT [ad_2] Source link

Power Grid to transfer assets worth Rs 7,500 crore to InvIT in FY23 Read More »

[ad_1] Chazz Huston Strategic Alliances Manager, Black Knight Secondary Marketing Technologies A few months ago, I started shopping for a new car. During this pursuit, I scoped out dozens of automaker and dealer websites to browse a wide variety of makes, models and price points. With so many choices out there, I dove into the process eager to compare cars and costs to narrow down the best options for my needs. Thanks to the fact that most auto retailers list their product and pricing online, this process was easy for me to complete on my own time. However, consider the sharp contrast between online vehicle shopping and the typical mortgage shopping experience. When customers expect complete transparency and convenience (think the Amazon experience), it’s remarkable most lenders have kept many of their current practices this long. While the mortgage point-of-sale experience has improved by leaps and bounds in recent years, the average shopping experience still leaves much to be desired. A Broken Shopping Experience Put yourself in your prospective customers’ shoes for a moment. You’re ready to purchase a home or refinance your loan, so you visit a few lender websites. You find customer testimonials, photos of the executive team and promises of a personalized mortgage experience. Typically, though, there’s something very important missing: the lender’s products and pricing. In fact, Black Knight examined hundreds of lender websites and found that just 32% make pricing readily available on their websites. Many lenders may find it difficult to buck tradition and publicize product pricing. But consumer expectations have changed – and they’re only going to continue to evolve. Lending institutions that fail to respond to changing consumer demands will, well, risk failure. When potential customers visit your website today, they are specifically looking to browse your products and pricing – just as if they were accessing any other type of retailer’s site. Data shows that consumers begin their mortgage shopping research 171 days before they complete an application. That means lenders have nearly six months to catch a prospective customer’s attention by simply making the information they want available. Failing to do so means these opportunities may be lost to lenders that do offer this basic information. After all, why would a customer want to disclose their Social Security number and other personal information to access rates from Lender A when they can review them instantly on Lender B’s website? Technology Ushers New Possibilities for Product and Pricing Fortunately, innovative technology and application programming interfaces (APIs) make it easy for lenders to seamlessly display accurate product and pricing information when and where their customers want it – from websites to self-service apps and everything in between. Thanks to APIs, consumers can now look for the best mortgage product and price on their own, whereas just a few years ago this task could only be completed by an originator. At Black Knight, we recognize the importance of enhancing the consumer shopping experience, and we’ve focused significant resources on helping our clients do just that. Our best-in-class Optimal Blue product, pricing and eligibility (PPE) engine serves as a utility for the industry by making product and pricing accessible from any solution throughout the lending life cycle. For example, through the power of APIs, our clients can embed a pricing widget on their homepage or within a customer-facing app. Additionally, Black Knight’s extensive partner network gives Optimal Blue PPE users the option to piece together a customized tech stack that meets their unique needs with turnkey integrations. The Time for Improvement is Now Tackling the issue of product and pricing transparency should be at the top of every lender’s to-do list. Fortunately, this challenge is easier to address than ever before thanks to modern technology. Beyond the significant benefits product and pricing transparency adds to the customer experience, enclosing rates across your lending ecosystem can help with sales, lead generation, conversion, back-office efficiencies, secondary marketing and more. Your prospective customers already expect it, and the technology is available to make it happen. Don’t risk falling behind the competition and losing business with “the way we’ve always done it” thinking. The post This one practice can help lenders stop losing customers appeared first on HousingWire. [ad_2] Source link

This one practice can help lenders stop losing customers Read More »

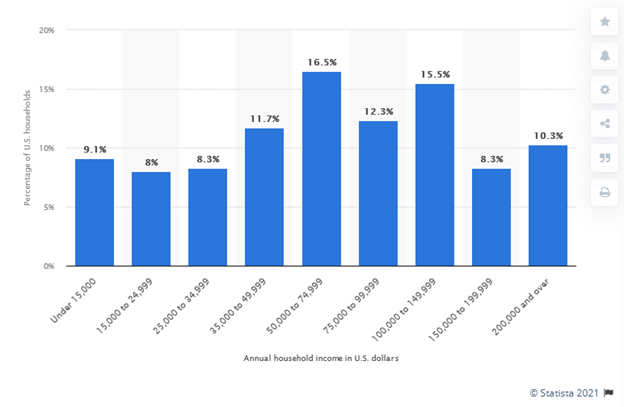

[ad_1] It’s often said that “numbers don’t lie”. If so, what does that reveal about personal finance in the USA? To answer that question, we’ve prepared this analysis of personal finance facts and statistics to help you understand approximately where you are in comparison with other Americans. The information revealed in our analysis isn’t intended to make you feel insecure in any way. Instead, it’s designed to help set parameters that will enable you to see how you are doing and to make improvements where you believe it’s necessary. We hope you like numbers because we have plenty of them! They’re a necessary evil, and they go with the territory when it comes to personal finance. We’re going to present statistics concerning multiple topics relating to income, debt, savings and budgeting, and financial planning. Income Median Household Income Per State The median household income nationwide is $79,900. But there is a wide variation between the individual states. The following median household income statistics are provided by the US Department of Housing and Urban Development, as of April 1, 2021: State Median Household Income Alabama $66,700 Alaska $93,900 Arizona $73,200 Arkansas $60,700 California $90,100 Colorado $93,000 Connecticut $102,600 Delaware $83,000 District of Columbia $123,100 Florida $70,000 Georgia $74,700 Hawaii $99,800 Idaho $69,000 Illinois $85,000 Indiana $73,300 Iowa $79,500 Kansas $77,400 Kentucky $65,100 Louisiana $64,700 Maine $75,700 Maryland $106,000 Massachusetts $106,200 Michigan $75,300 Minnesota $93,100 Mississippi $60,000 Missouri $72,300 Montana $72,100 Nebraska $79,400 Nevada $75,100 New Hampshire $98,200 New Jersey $106,000 New Mexico $61,400 New York $87,100 North Carolina $70,900 North Dakota $90,100 Ohio $75,300 Oklahoma $67,000 Oregon $81,200 Pennsylvania $81,000 Rhode Island $88,000 South Carolina $68,700 South Dakota $75,500 Tennessee $68,600 Texas $75,100 Utah $85,300 Vermont $84,100 Virginia $93,000 Washington $91,600 West Virginia $60,300 Wisconsin $80,300 Wyoming $81,900 US $79,900 What Percent of People Represent the Highest Incomes in USA Have you ever wondered where your income falls among wage earners nationwide? For example, you may be interested to know that if your household income is over $200,000 per year, you’re among the 10.3% wealthiest households in the country. According to Statista, the income distribution in the US is as follows (for 2019): How many Americans Live Below the Poverty Line? According to the U.S. Census Bureau, 10.5% of the population – or about 34 million people – were below the poverty line in 2019. According to the US Office of the Assistant Secretary for Planning and Evaluation (ASPE) the poverty line for 2019 is as follows (based on annual income by household size) for most of the country: One person – $12,490 Two people – $16,910 Three people – $21,330 Four people – $25,750 Five people – $30,170 Six people – $34,590 Seven people – $39,010 Eight people – $43,430 Top 5 Richest States in the USA Based on the table for “Median Household Income Per State” provided by the US Department of Housing and Urban Development in the first section above, the top five richest states in the USA are: Massachusetts, $106,200 Maryland, $106,000 New Jersey, $106,000 Connecticut, $102,600 Hawaii, $99,800 Top 5 Poorest States in the USA Based on the table for “Median Household Income Per State” provided by the US Department of Housing and Urban Development in the first section above, the top five poorest states in the USA are: Mississippi, $60,000 West Virginia, $60,300 Arkansas, $60,700 New Mexico, $61,400 Louisiana, $64,700 Income Per Education Level According to the Bureau of Labor Statistics (BLS), income per education level is as follows (for 2017): Education Level Mean usual weekly earnings Annual earnings Doctoral degree $1,743 $90,636 Professional degree $1,836 $95,472 Master’s degree $1,401 $72,852 Bachelor’s degree $1,173 $60,996 Associate’s degree $836 $43,472 Some college, no degree $774 $40,248 High school diploma, no college $712 $37,024 Less than a high school diploma $520 $27,040 Average for all education levels $907 $47,164 Median Earnings by Age Bracket According to the US Bureau of Labor Statistics, median earnings by age bracket are as follows (for the second quarter of 2021): Age Bracket Mean usual weekly earnings Annual earnings 16 to 24 $619 $32,188 25 to 34 $928 $48,256 35 to 44 $1,119 $58,188 45 to 54 $1,134 $58,968 55 to 64 $1,130 $58,760 65 and over $989 $51,428 Debt Average Annual Consumer Spending in the USA Average annual consumer spending in the USA was $63,036 in 2019, according to the Bureau of Labor Statistics. The biggest individual category expenses were: Housing, $20,679 Transportation, $10,742 Food, $8,169 Personal insurance and pensions, $7,165 Health, $5,193 Total Consumer Debt in the USA Total consumer debt in the USA is $14.96 trillion. Those are the statistics issued by the Federal Reserve Bank of New York for the second quarter of 2021. That includes all forms of consumer debt, including home mortgages, student loans, credit cards, and auto loans. Amount of Credit Card Debt in the USA The amount of credit card debt in the USA is $807 billion. Average credit card debt per family is $6,270, and 45.4% of families carry some amount of credit card debt. (Source: Value Penguin) How Many Americans Know How Much They are Paying in Credit Card Interest? The average American household pays $1,045.55 in credit card interest each year. It’s entirely likely the average American has no solid idea how much he or she is paying, due to multiple credit cards, and the variable nature of both credit card balances and interest rates. How Many Car Repossessions Happen Yearly in the USA About 2 million car repossessions yearly in the USA (source: Etags.com). Vehicles are typically repossessed within 90 days of loan default (your last payment). Total Amount of Student Loan Debt in the USA The total amount of student loan debt in the USA is a record $1.71 trillion as of the beginning of 2021 (source: StudentLoanHero.com). 44.7 million students and graduates owe an average of nearly $30,000 in student loan debt. But student loan debts taken by parents for the benefit of their children averaged $37,200

Personal Finance Facts and Statistics Read More »

[ad_1] If you love Brooks Running Shoes, don’t miss this rare discount! Zulily is having a big Brooks Running Shoes Sale right now! Plus, you’ll get an exclusive 15% additional discount at checkout as our reader! These are RARE discounts on Brooks brand! Hurry – these are selling out VERY quickly. Shipping starts at $5.99. But if you place one order today, the rest of your orders will ship for FREE through 11:59 p.m. PT tonight! [ad_2] Source link

Huge Brooks Running Shoes Sale + Exclusive 15% Additional Discount! Read More »

[ad_1] Former U.S. Senator Dole to lie in state in U.S. Capitol Rotunda Thursday [ad_2] Source link

Former U.S. Senator Dole to lie in state in U.S. Capitol Rotunda Thursday Read More »