Biden asks U.S. Supreme Court to hear 'Remain in Mexico' case

[ad_1] Biden asks U.S. Supreme Court to hear 'Remain in Mexico' case [ad_2] Source link

Biden asks U.S. Supreme Court to hear 'Remain in Mexico' case Read More »

[ad_1] Biden asks U.S. Supreme Court to hear 'Remain in Mexico' case [ad_2] Source link

Biden asks U.S. Supreme Court to hear 'Remain in Mexico' case Read More »

[ad_1] By Naveen Aggarwal A central theme of the tax policies of the current dispensation is addressing ambiguities in income-tax (I-T) laws that have led to tax disputes. To this end, two amendments in 2021 hold prominence. On the administrative front, the government has completely revamped the procedure and conditions to re-assess a taxpayer’s income. The time limits for initiation of reassessment have also been changed with a longer period of 10 years available only in limited circumstances. Hopefully, this will help increase certainty for the taxpaying community. Second, India buried the ghost of the retrospective amendment on indirect transfer of shares which was brought in to sidestep the Supreme Court’s judgement in a landmark case. In August, the government brought in legislation which effectively exempts indirect transfer of shares pursuant to transactions undertaken prior to May 28, 2012, from taxation. While it may be argued that India could have avoided the spate of litigation in Indian and international forums by effecting such a change much earlier, this move was a larger policy statement that India is not in favour of retrospective changes to its I-T laws. With any change in law—especially tax laws—divergence in interpretation is common. With India progressively changing tax laws, the judiciary had to repeatedly step in to address these aspects. For instance, while the reassessment process has changed from April 1, 2021, Revenue issued notices for past years without following the laid-out process. Taxpayers approached High Courts, with mixed results. Similarly, as faceless assessment settles in, taxpayers have had to approach the courts, on grounds of natural justice due to the lack of an opportunity of being heard. Dividend distribution tax, abolished in 2020 and replaced with withholding tax, brought in new nuance before the judiciary as disputes have arisen between the Revenue and taxpayers over the applicability of the Most Favoured Nation clause in certain tax treaties. The outgoing year also saw a Supreme Court judgement resolving the decade-long dispute on taxability of cross-border supply of software. The apex curt was faced with resolving a technology-driven issue: the supply of software, first via floppy disks, then CDs to now being hosted and accessed digitally. The Supreme Court evaluated four different business models and dived deep into Indian copyright laws, tax amendments and tax treaty provisions, and only then provided a clear verdict. This has impacted many taxpayers and will, in addition to settling the issue on characterisation of software payments, also serve as a reiteration of the principle that tax treaty provisions prevail over unilateral domestic amendments that impact non-residents. Non-residents continue to tackle the varied interpretational issues due to India’s unilateral measure to tax the digital economy, via the equalisation levy (EL). There had been a general proliferation of similar unilateral measures by countries. However, EL provisions—although clarified to an extent in Budget 2021—are wider in ambit and continue to pose challenges in terms of coverage of routine cross-border transactions. However, in October, after multiple rounds of engagements, 136 countries, representing more than 90% of the global GDP, have signed on to the OECD framework which will revolutionise how cross-border income of multi- national enterprises is to get taxed. The Two Pillar approach aims to ensure that the world gradually moves away from taxation based on physical presence, MNEs don’t use jurisdictions merely for tax arbitrage and countries are dissuaded from the race to the bottom in offering low tax rates to attract investment. With a global minimum tax of 15% under Pillar Two and market jurisdictions’ right to receive a proportionate share of profit, irrespective of physical presence, under Pillar One, a clearly defined path for the implementation of the Two Pillar approach in the coming years has been laid, with a commitment on withdrawal of unilateral measures like the EL. If 2021 was a trailer, 2022 will likely be the blockbuster as countries negotiate and implement changes to bring to life the new international tax rules. While the withdrawal of EL is not likely next year, with India reaching an interim compromise with the US for a credit mechanism of EL against the OECD Pillar One liability of in-scope US-headquartered entities, one is hopeful that the government would consider the concerns raised by the industry and issue the necessary guidance. Additionally, developments in international tax would require recalibration of Indian tax laws to give effect to the OECD framework. With the government planning to introduce laws to regulate crypto currencies, taxation of crypto and other digital assets is going to take centrestage. Amidst all this, against the backdrop of the success of one-time dispute settlement schemes such as ‘Vivad Se Vishwas’ and the Government’s objective to cut down tax litigation, the coming year may be an opportune time for the government to consider a permanent mechanism to settle tax disputes which shall supplement the changes to the tax assessment regime. The author is Partner (Tax) KPMG in India [ad_2] Source link

Tax in 2021, and what’s likely in 2022 Read More »

[ad_1] A bullish housing market What a year 2021 has been. We started the year with many pundits saying that the U.S. economic recovery was a false story and that we were about to embark on a second housing bubble crash due to forbearance. However, not only did the U.S. economy continue to recover from the lows of April of 2020, but the 2021 economic data shows it has been one of the hottest years in many decades. Retail sales have been off the charts, job openings are at 11 million, GDP growth picked up big time and jobless claims hit a level last seen in 1969. The housing market didn’t crash at all, in fact, more Americans bought homes with mortgages in 2021 than in 2020. The housing crash addicts in America have now been wrong for a decade. After failing from 2012-2019, they went all in during 2020 due to COVID-19, only to move the goalpost to 2021 due to forbearance. That didn’t end well for them. Now that we are just a few days away from 2022, it’s time to take a look at the positive and the negative housing stories of 2021. The good Keeping it simple, mother demographics is the most powerful economic force in the world. I’ve been writing for many years that years 2020-2024 would have the best housing demographics ever recorded in history. During this timeframe we have a historic one-time bump in ages 28-34 — the peak age for home buying. In fact, the reason the housing bears have such terrible track records is because they look at housing as an investment first, not the cost of shelter to a person’s capacity to own the debt. First and foremost, Americans are buying a place to live, not an investment. With only one existing home sales report left this year, it is imperative to focus on the fact that more Americans bought homes in 2021 than 2020. These households got sub-3.5% mortgage rates, so on the mortgage rate side of the equation, it’s never been better. Also, post-2010, the loans in American are very vanilla on the debt structure side of the equation. Housing demand itself is slightly outperforming what I would have expected in 2021 as existing home sales have had a few prints over 6.2 million toward the end of the year. Today, NAR‘s pending home sales report came out showing a slight decline, but the trend here is also better than what I thought it would be toward the end of the year. Housing permits are growing and this is a good thing for the economy and construction jobs. While I have never been a housing construction boom guy because mature economies typically don’t have a construction boom, the fact that permits are keeping their uptrend is a big positive for the United States of America. We do have some very positive stories about the housing market in 2021, but not all is perfect, of course. The bad My economic models over the years showing that housing demographics would be better in the years 2020-2024 have also led me to be mindful of home-price growth taking off. Currently, home-price growth is too hot, which is why I label this the unhealthiest housing market post-2010. According to the parameters I set for this period, as long as nominal home-price growth was only 23% or less during this unique five years, then it would be manageable considering the demographic backdrop and low mortgage rates. Well, it looks like my five-year growth model has been taken out in two years. Not the best of news as we start year three of that time period with a solid possibility of new all-time lows in inventory this spring. While I do believe the rate of home-price growth is cooling off — since data from the S&P CoreLogic Case Shiller Home Price Index lags — the market is still seeing home-price growth above my five-year price model, so wishing for less price growth in 2022 is a must for me. Simply put, the days on market are still too low, which creates unhealthy price growth, too much bidding action for homes, and a lot of stress in the home-buying process. Another aspect that doesn’t get enough attention because it’s a hard look in the mirror: We all get greedy when we have pricing power — it’s the nature of the beast. Home sellers strive to get the highest price from the best offers and homebuilders have the pricing power over consumers. Since housing is a shelter cost — everyone needs a home to live in — it’s much different than buying a stock. As we can see below, the builders are maximizing their pricing power. Even with all the labor and material costs they have had to deal with since the pandemic started, they had a stellar year with their profit margins. Yes, the housing market has done well during 2020 and 2021, but it has come at a price and with rental inflation kicking into another gear, the cost of shelter rising is a theme for 2022. The excellent Wait, isn’t it “The Good, the Bad and the Ugly?” Not in my western 2021 world! We write history on our own terms and we do have some excellent news. Going into 2021, the big question mark was what would happen with forbearance. Now, for me, it wasn’t such a big question mark. I was so confident that forbearance wasn’t going to be the doomsday event that many American and housing bears were rooting for during this pandemic that I coined the term forbearance crash bros in the summer of 2020. This was in honor of all the trolling, non-economic people on the internet calling for housing to crash when clearly none of these people had any clue about the housing market or the credit debt structures of homeowners post-2010. I documented my work with many articles, which can be found here. Forbearance went from

The 2021 housing market recap by Logan Mohtashami Read More »

[ad_1] You can get a free 2022 calendar! Sign up for a FREE 2022 DeLallo Calendar! Thanks, Freebie Shark! [ad_2] Source link

Free 2022 DeLallo Calendar Read More »

[ad_1] Purdue bankruptcy judge extends temporary litigation shield for Sacklers [ad_2] Source link

Purdue bankruptcy judge extends temporary litigation shield for Sacklers Read More »

[ad_1] By Anuj Bhatia, Shruti Dhapola & Nandagopal Rajan iMac M1The new Apple iMac is an all-in-one desktop computer that takes cues from the original iMac of the late 90s but is still the most forward-looking device for your work space. The iMac combines a surprisingly good 24-inch screen with more than capable performance (all thanks to the M1 processor) and has a 1080p webcam that makes it more than relevant in the pandemic year. Apple 16-inch MacBook ProThe 16-inch MacBook Pro is the most powerful laptop Apple has ever created. If you are willing to pay the price, you will not be disappointed. Not only is the 16-inch MacBook powerful enough for heavy computing tasks, it also fixes all the issues the creator community had with the previous generation model. Configurable with either the M1 Pro or M1 Max, the 16-inch MacBook Pro becomes a poster boy of Apple’s latest silicon. The new MacBook Pro promises plenty of ports, a great keyboard, and a bright and colourful Liquid Retina XDR display that can reach 1,000 nits when playing HDR content. Dell XPS 13Dell’s XPS 13 has consistently been ranked high among the premium laptops. The bezel-free 16:10 display is gorgeous, the design is top-notch, performance is unmatched, and the keyboard and the battery are its strengths. It can cope with everything from web browsing to light video editing and everything in between. Although the XPS 13 is the benchmark in the high-end Windows laptop segment, its port selection is a bit disappointing and the 720p webcam is meh. The 2021 XPS 13 is a sign of Dell making things right. HP Pavilion Aero 13The Pavilion Aero 13 is one of the best ultrathin-and-light Windows laptops on the market, finding a perfect balance between business and fun if you are still working remotely. Although the Pavilion lineup is largely limited to value-for-money notebooks, the Aero 13 gets a lot of premium features including magnesium-aluminum chassis, long battery life, the performance from the AMD Ryzen 5 5600U is impressive, and bright and colourful display. It makes us wonder how HP packed in so many features in a notebook that weighs just 970 grams. In a way, HP has made a MacBook Air rival and it succeeds to some extent. [ad_2] Source link

The best gadgets of 2021- PCs: Back in relevance Read More »

[ad_1] Covid-19, Omicron Variant and Testing News: Live Updates The New York Times U.S. Covid cases rise to pandemic high as delta and omicron circulate at same time CNBC New COVID-19 cases in US soar to highest levels on record Associated Press World hits record number of COVID-19 cases in a week: Tally Al Jazeera English The latest on coronavirus pandemic and Omicron variant: Live updates CNN View Full Coverage on Google News [ad_2]

Covid-19, Omicron Variant and Testing News: Live Updates – The New York Times Read More »

[ad_1] This article is part of our HousingWire 2022 forecast series. After the series wraps early next year, join us on February 8 for the HW+ Virtual 2022 Forecast Event. Bringing together some of the top economists and researchers in housing, the event will provide an in-depth look at the predictions for next year, along with a roundtable discussion on how these insights apply to your business. The event is exclusively for HW+ members, and you can go here to register. Steve Berneman is the rare startup founder who wants his industry to shrink, not grow. “One of our big goals at Blueprint Title is to shrink the title insurance business from an $18 billion business to a $10 billion business,” Berneman, the company co-founder and CEO. “We believe that title insurance premiums are significantly too high and that if underwriters and agents were more efficient and took a different approach to the market, they wouldn’t have to charge as much.” To that end, Berneman’s Nashville-headquartered company recently launched a portal that allows real estate professionals and their clients to keep track of the title process. And Blueprint acquired an underwriter as it attempts to gain market share in an industry known for extreme barriers to entry. Blueprint may ooze ambition, but it is just one among dozens of tech-forward startups in the title industry, all of whom are competing for a slice of the 10.5% share of the market controlled by small, independent title insurance companies. For this reason, John Campbell, a title insurance industry analyst at investment bank Stephens Inc., doesn’t feel that the “Big Four,” namely Fidelity National Title, First American Financial, Old Republic Title and Stewart Title, who as of the second quarter of 2021 controlled 80.3% of the market, should be too concerned about the rise of the little guy. But they won’t be resting on their laurels, either. “A lot of the major firms are increasingly becoming more tech savvy and they are using that tech to become a bit more integrated within the broader real estate transaction ecosystem,” Campbell said. Whether big or small, title companies are deploying technology to improve the flow and ease of the entire closing process. Two of the biggest developments have been the phenomenal growth of remote online notarization (RON) and document management platforms. Stewart has worked to expand its online signing and closing capabilities, which it plans on beefing up in the new year, said company president Tara Smith. And First American has launched its own suite of digital interfaces and platforms: IgniteRE allows real estate professionals to manage all components of the transaction in one place; and Docutech, which was acquired in 2020, enables lenders to deliver a more seamless eClosing experience. Many of the larger firms are also increasing their level of automation in order to take on more volume and maintain their lead over the plucky startups. “All of the firms have become a lot more automated,” Campbell said. “I don’t think there is any way you can deliver orders with the type of growth they have all seen relative to their head count, so due to this you are seeing a lot more automation.” First American is among the “Big Four” that has really embraced the use of automation, especially to tackle refinance transactions, which have boomed over the past year due to low interest rates. “Today, 96% of our refinance transactions run through our automated title decision engine,” Chris Leavell, the COO of First American, said. “Based on our own risk profile, we’ve achieved a fully automated underwriting decision on 50% of those orders, and we are semi-automated on an additional 40%.” Looking ahead, Leavell says that First American hopes to introduce some level of automation to purchase transactions. Although automation is helping keep up with a huge increase in title insurance premium volume, the industry is still reckoning with a talent crunch. Back in 2014 the average age of a title agent or broker, according to industry statistics, was 60. That hasn’t changed over the past seven years. Smith feels that this talent shortage is one of Stewart’s biggest challenges. “We are all competing for the same talent, so we have decided to focus on the opportunity to bring new talent into the industry,” Smith said. “We have an annual intern program in which we focus on bringing people into the organization and helping them learn the industry from the ground up.” Despite what seems like an impenetrable industry faced with numerous challenges, DOMA, formerly known as States Title, has found some success in leveraging its technology to increase market share. In its ongoing effort to consolidate and speed up the closing pro-cess, DOMA has its sights on becoming a one-stop-shop for closing a purchase. “We would like within the next five-to-10 years for somebody to be able to sign a purchase contract for a home on a Friday evening and move in on a Monday morning,” Max Simkoff, the CEO of DOMA, said in an interview. In order to achieve this goal, Simkoff is working to grow DOMA’s current technological offerings and is looking to expand into the lending and appraisal space. While this does seem like a far-off dream, Campbell believes DOMA is not alone in wanting to become a one-stop shop. Compass, the nation’s second-largest real estate brokerage, and Rocket Mortgage, easily the biggest lender, are among the massive real estate companies with growing title segments. Others are sure to follow. “Everyone is looking at that value chain in the home buying process that once looked very distinct as much as 10 years ago, but now the lines are just blurring on all sides and I think we will continue to see that,” Campbell said. This article was first featured in the Dec/Jan HousingWire Magazine issue. To read the full issue, go here. The post The “Big Four” take on the upstarts in title insurance appeared first on HousingWire. [ad_2] Source link

The “Big Four” take on the upstarts in title insurance Read More »

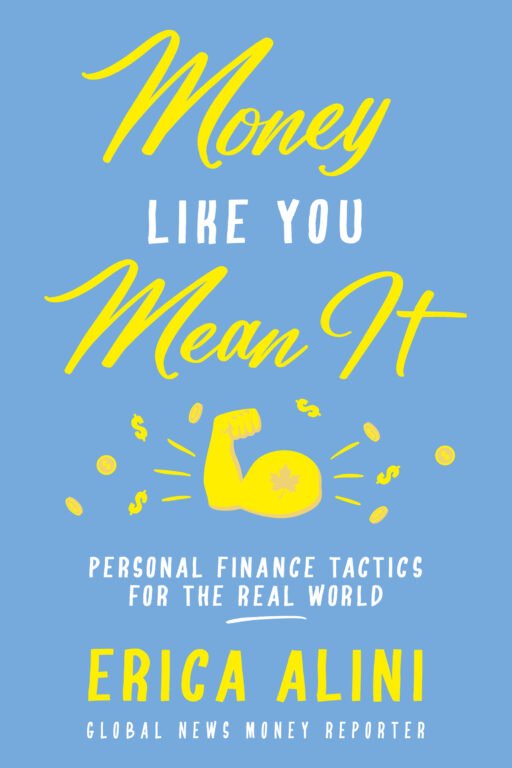

[ad_1] The best personal finance books are engaging, entertaining and even enlightening, changing the way we think about and manage our money. Here are some of our top picks. Money Like You Mean It by Erica Alini Dundurn Press; softcover $21.99, e-book $8.69 It’s evident the idea for Money Like You Mean It, a comprehensive guide for millennials and Gen Z to mastering personal finance in the current economy, was hatched well before the pandemic. It starts from the assumption that if you’re a young adult living in Canada, you’re likely struggling—to navigate debt, to earn a stable income, to imagine being able to “get a job, work hard, spend less than you save, and retire at 65,” as author Erica Alini puts it. Frankly, for many young people, that hasn’t felt true in years. But the fact that the book comes on the heels of a pandemic that has further disrupted our hopes regarding money, the housing market and our jobs makes it all the more relevant and useful to a generation searching for traditionally middle-class comforts. Alini, the personal finance reporter at Global News and a self-described “older millennial,” pulls from personal experience and a decade of money reporting to compile practical tips for young people on everything from taming debt, investing and making sense of buy-now, pay-later options to saving for retirement, navigating the gig economy and negotiating a (long-overdue) raise. Alini sees a generation that has struggled to make sense of their financial lives. Her book offers a compass to get through the “daunting, overgrown jungle” of personal finance today.—Justin Dallaire Rich Girl, Broke Girl by Kelley Keehn Simon & Schuster; softcover $22.99, e-book $9.99 If you can’t keep your eyes open while reading a personal finance book but have no problem devouring tales of financial woe on, say, Reddit, this book is for you. Kelley Keehn—a Canadian personal finance educator and best-selling author of Talk Money To Me—writes about finance with a people-first approach. Through anecdotes about real women, she sheds light on common financial pitfalls and gives solutions for how to avoid and overcome them. Stories of women who struggled to pay off credit card debt, who let partners control their finances and who let fear keep them from taking financial risks serve as a springboard for Keehn to discuss things like budgeting, investing, tax shelters and financial planning. While anyone can benefit from these takeaways, Keehn wrote this book for women. Why? In Canada, women control one-third of the country’s financial assets, and this figure is set to grow. Even so, younger generations are taking less initiative when it comes to their finances. And, as Keehn recounts, when women take less initiative with their finances, repercussions may follow—for instance, two-thirds of women whose partners are the primary breadwinner feel trapped. Through relatable stories and a strong dose of judgment-free wisdom from Keehn, readers will become more aware of their money missteps and more empowered to take control of their financial futures.—Courtney Reilly-Larke House Poor No More by Romana King Houndstooth Press; softcover $13.99, e-book $8.99 Romana King is the friend you wish you had when buying a house, dealing with repairs—or, really, anything involving money and your home. In her new book, she sounds like a calm, cool confidante who’s been there, done that. In a nutshell, the book is about the value of your home. King explains that it’s not just about the listing price, the rebuild price or even the market value. She walks us through how a home can be a long-term investment, if you look at the numbers right: from bidding wars to down payment funds (what she calls saving for a down payment) to insurance to repairs to utility costs to managing debt. It’s a lot, but that’s what makes House Poor No More a helpful guide for first-time home buyers or even those higher up on the real estate ladder. Essentially, King gives you the long-term picture and puts all the costs into perspective. Need a new roof? The quotes are big enough to have you questioning home ownership. But all those large expenses (and the little ones, too) have a purpose in growing and maintaining your home’s value. Having read the book, I already feel more confident about talking to contractors. The key, though, is the numbers. King gives current average costs for everything. Every. Thing. This book will be a resource for years to come—you’ll just need to update the numbers.—Lisa Hannam Broke Millennial Talks Money by Erin Lowry TarcherPerigee; paperback $22, e-book $13.99 As someone who’s 22 and new to the confusing and often crazy world of personal finance, I can attest to the fact that talking about money is extremely difficult. Luckily, Erin Lowry—the best-selling author of Broke Millennial and Broke Millennial Takes On Investing—has advice to make it less awkward, and her writing is so down-to-earth and engaging that even a financial novice like me can understand. Her new book reads as if you’re having brunch with a long-time friend you can talk to about anything, including the often taboo topic of personal finance. Lowry shares ideas for talking about money with co-workers, romantic partners, friends and family. With friends, for example, should you share your salary and net worth—and what if your money situations are really different? One of the hardest-hitting lessons I learned is that “context, context, and context” (as Lowry puts it) means everything when discussing income with friends. Before sharing your numbers, she says, ask yourself why you’re doing it. Are you providing insight to motivate a friend to get out of debt or negotiate a raise, or are you flaunting what you’ve got? Lowry not only arms you with a variety of personal finance tips but also challenges you throughout the book. One example: send out a few emails to your co-workers asking about their respective salary ranges, so you can better negotiate a raise. Another simple yet effective challenge: practice at least two negotiation strategies.

New year, new money habits: 5 personal finance books for a fresh start Read More »

[ad_1] The post What Is Direct Lending? A Beginner’s Guide appeared first on Millennial Money. Direct lending is becoming increasingly popular due to the higher interest rates it can yield for investors. In its basic form, direct lending involves providing credit directly to small and mid-sized businesses that use the money for expansion. Keep reading to learn all about how direct lending works, the different types of options and companies on the market, and how to potentially benefit from it. Direct Lending: An Overview The Role Investors Play How Direct Lending Works How to Invest with Direct Lending The Pros and Cons of Direct Lending for Investors Direct Lending: An Overview Following the 2008 financial crisis, many banks stopped lending to lower and middle-market companies in favor of large corporations with stronger cash flows and collateral. The sluggish economy and new regulations made it very difficult for small, private companies to receive mission-critical loans. This gave rise to direct lending, a strategy in which private lenders — or non-banks — make loans to companies while avoiding intermediaries. Non-bank lending is similar to private equity, as it involves raising funds from outside investors. Direct lending is appealing for many companies because it avoids regulatory restrictions. That means direct lenders don’t have to meet stringent lending qualifications. Through direct lending, it’s fast and easy for small organizations to build capital structure. As such, direct lending is expected to remain in high demand for the foreseeable future. If nothing else, it’s an interesting option for investors who want to diversify their asset allocation by injecting capital into other businesses. The Role Investors Play Investors fuel the direct lending process by issuing capital to third-party fund managers or platforms, helping to finance private loans. Direct lending funds may also draw capital from business development companies and asset management firms. When you issue funding as an investor, you can help fund part or all of a loan, with the goal of earning strong and consistent returns from higher-than-average interest rates. In exchange, there are some fees to consider. For example, direct lending often comes with an incentive fee, calculated based on the fund’s performance over time. In addition, investors often likely have to pay a management fee when working with a direct lender. It’s critical to read a fund’s prospectus before getting started to understand the various fees that will come into play throughout the course of the loan. Watch out for early termination fees and exit fees if you decide to reclaim your capital. Pricing should also be a big determining factor when selecting a direct lending provider. How Direct Lending Works In most cases, a direct lender raises money from a network of investors and partners. After securing funding, the lender will approach a potential borrower and make a leveraged loan offer. If you’re new to this term, a leveraged loan is simply a commercial loan funded by multiple investors. There are three ways a direct lender may offer a loan to a borrower: 1. First lien In a first lien agreement, the borrower agrees to pay off the loan before paying off all other debt classes. 2. Second lien A second lien agreement requires paying off a loan after a senior lien or a claim on a property. 3. Unitranche debt With a unitranche agreement, senior and junior debt combine into a single loan with a mixed interest rate and a predictable repayment schedule. Is direct lending the same as private debt? In a direct lending agreement, an asset manager sells the loan to many different investors. In a private debt arrangement, a single investment bank funds the loan. Private debt also deals with a much wider range of financing, such as distressed debt and mezzanine financing. How to Invest With Direct Lending There are two ways to begin a direct lending investment strategy. You can either work with a direct lending provider who handles the process end-to-end or source borrowers yourself using a peer-to-peer lending service. Working with a direct lending provider The most common approach involves partnering with a direct lending provider. Again, this option requires paying fund management and incentive fees. However, the tradeoff is that management teams handle all the legwork of sourcing and vetting the borrower and managing the relationship. All you have to do as the investor is provide funding. Top direct lending providers for 2021 The following companies offer direct lending opportunities for investors, with qualifications varying from provider to provider. Be sure to check with the provider in advance to determine eligibility. Apollo Apollo launched Apollo Strategic Origination Partners in 2020. The platform aims to provide roughly $12 billion in finance over the next three years to help meet corporate demand for direct origination. Blackstone Blackstone offers loans that are privately originated, senior secured, and with floating rates to middle-market companies across the U.S. and Europe. Blackstone also recently announced Blackstone Private Credit Fund (BCRED), a non-listed business development company (BDC) offering individual investors access to private credit through a continuously offered fund structure. Oaktree Capital Oaktree is a leading alternative investment management firm with a long history extending back to 2001. Today, the company issues senior and junior loans to a wide variety of private equity or independent companies. Intermediate Capital Group Intermediate Capital Group (ICG) invests in senior secured and subordinated debt instruments for companies throughout Europe. Investing through P2P The other option is to bypass large fund providers and go through peer-to-peer (P2P) investment service providers. P2P lending — or crowdsourcing — is becoming increasingly popular because it makes investing faster and easier than working with fund managers. Most P2P direct lending apps come with a robust platform that matches you directly with individual investors and business owners. As an investor, you can typically access a variety of metrics before deciding whether to invest in the organization. Then, when you find a match, you can usually fund a portion or all of the investment. P2P providers also have varying eligibility

What Is Direct Lending? A Beginner’s Guide Read More »