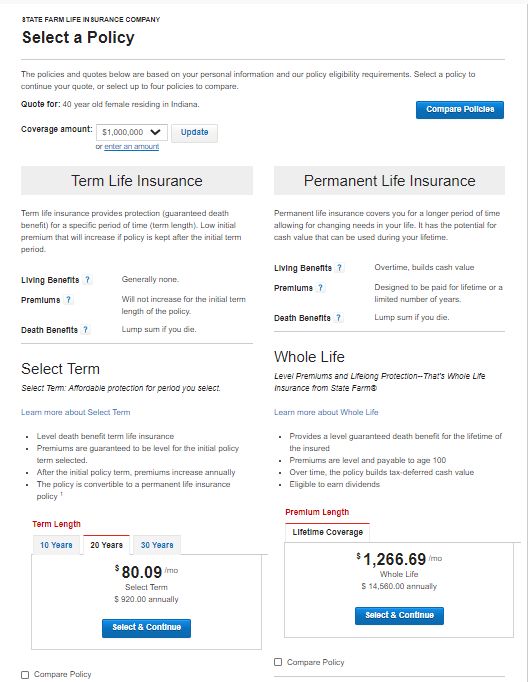

[ad_1] #mainContent a,#mainContent h3{font-weight:500!important}#mainContent h2{margin-top:3em;}#mainContent h3{margin-top:2.5em}#mainContent h3 span{font-weight: 300;letter-spacing:1px;}#mainContent h2{border-left:4px solid #3696da;padding:7px 0 7px 11px}ul.toc,ul.nextSteps{margin:.75em 0;list-style:none}ul.toc{padding:0 3.5em 2em; background:#f4f4f4;margin-top:0;border-left:4px solid #3696da;}ul.nextSteps{padding:0 .85em;margin-bottom:0px;margin-top:0}ul.toc li:before,ul.nextSteps li:before{content:””;border-style:solid;display:block;height:0;width:0;position:relative}ul.toc li:before{border-color:#3696da transparent transparent transparent;border-width:.35em .5em 0 .5em;left:-1.5em;top:.8em}ul.nextSteps li:before{border-color:transparent #ffab00;border-width:.5em 0 .5em .35em;left:-.85em;top:1.12em}#mainContent ul.toc li a,#mainContent ul.nextSteps li a{color:rgb(33,33,33);font-weight:300!important}#mainContent ul.nextSteps li a{border-bottom:2px solid #ffab00}#mainContent ul.nextSteps li a:hover{background:rgba(255,171,0,.3);text-decoration:none}<br /> Do you think a million-dollar term life insurance policy sounds like too much insurance? As a Certified Financial Planner, I see underinsured people every day. What do I tell them? A million-dollar term life insurance policy might actually be the minimum coverage needed for the typical middle-class household, but it’s affordable. That might sound like an exaggeration, but if you crunch the numbers – just as we’ll be doing a little bit – you’ll realize that a million-dollar policy might be just what you need. The good news is term life insurance isn’t nearly as costly as most people think. What makes term even better is that larger policies cost less on a per thousand basis than smaller policies do. You may find the premium on a $1 million policy is only a little bit higher than it is for $500,000. 503 Service Temporarily Unavailable 503 Service Temporarily Unavailable cloudflare Do You Really Need a $1 Million Term Life Insurance Policy? Probably, but let’s find out. A general rule of thumb is that you should get 10x your income as baseline coverage for life insurance. If you’re young, that may be low because you may want to provide your family with enough to replace your income for 15 years or more. Today, $1 million has become the new baseline for life insurance by a primary breadwinner. Anything less could leave your family financially impaired. Typical obligations to add when calculating the amount you need Here’s a list of all the different obligations you may want to have life insurance cover in the unfortunate event you pass away early. Your income (and for how many years) Your final expenses Any debt you may want to be settled Future obligations such as college for children Other obligations such as business Typical items you can subtract when calculating the amount you need Current life insurance policies Assets (like cash or stock) you might choose to use instead of life insurance Now that you have an idea of these obligations, let’s punch them into this life insurance calculator to find out if you need a million-dollar policy. if( typeof fbuilderjQuery == ‘undefined’) var fbuilderjQuery = jQuery.noConflict( ); /* <![CDATA[ */ var cp_calculatedfieldsf_fbuilder_config_1={"obj":{"pub":true,"identifier":"_1","messages":{"required":"This field is required.","email":"Please enter a valid email address.","datemmddyyyy":"Please enter a valid date with this format(mm/dd/yyyy)","dateddmmyyyy":"Please enter a valid date with this format(dd/mm/yyyy)","number":"Please enter a valid number.","digits":"Please enter only digits.","max":"Please enter a value less than or equal to {0}.","min":"Please enter a value greater than or equal to {0}.","previous":"Previous","next":"Next","pageof":"Page {0} of {0}","minlength":"Please enter at least {0} characters.","maxlength":"Please enter no more than {0} characters.","equalTo":"Please enter the same value again.","accept":"Please enter a value with a valid extension.","upload_size":"The file you've chosen is too big, maximum is {0} kB.","phone":"Invalid phone number.","currency":"Please enter a valid currency value."}}}; /* ]]> */ form_structure_1=[[{“form_identifier”:””,”name”:”fieldname3″,”shortlabel”:””,”index”:0,”ftype”:”fcurrency”,”userhelp”:”Enter your annual income, before taxes. Do not include income from your spouse or other members of your household.”,”userhelpTooltip”:false,”csslayout”:””,”title”:”Annual Income”,”predefined”:””,”predefinedClick”:false,”required”:true,”readonly”:false,”size”:”small”,”currencySymbol”:”$”,”currencyText”:””,”thousandSeparator”:”,”,”centSeparator”:”.”,”noCents”:false,”min”:””,”max”:””,”formatDynamically”:true,”fBuild”:{},”parent”:””},{“form_identifier”:””,”name”:”fieldname13″,”shortlabel”:””,”index”:1,”ftype”:”fslider”,”userhelp”:”We suggest a minimum of 5 years. If you have kids, consider covering them until they are adults.”,”userhelpTooltip”:false,”csslayout”:””,”title”:”How many years should coverage last?”,”predefined”:”5″,”predefinedMin”:””,”predefinedMax”:””,”predefinedClick”:false,”size”:”small”,”thousandSeparator”:”,”,”centSeparator”:”.”,”min”:”1″,”max”:”30″,”step”:1,”range”:false,”caption”:”{0}”,”minCaption”:””,”maxCaption”:””,”fBuild”:{},”parent”:””},{“form_identifier”:””,”name”:”fieldname4″,”shortlabel”:””,”index”:2,”ftype”:”fcurrency”,”userhelp”:”The total value of all liquid assets (bank and investment accounts). Do NOT include retirement accounts like 401(k)s or IRA.”,”userhelpTooltip”:false,”csslayout”:””,”title”:”Assets”,”predefined”:””,”predefinedClick”:false,”required”:true,”readonly”:false,”size”:”small”,”currencySymbol”:”$”,”currencyText”:””,”thousandSeparator”:”,”,”centSeparator”:”.”,”noCents”:false,”min”:””,”max”:””,”formatDynamically”:true,”fBuild”:{},”parent”:””},{“form_identifier”:””,”name”:”fieldname5″,”shortlabel”:””,”index”:3,”ftype”:”fcurrency”,”userhelp”:”Optional. Add an amount here if you want your life insurance to provide funds for your kidsu2019 education.”,”userhelpTooltip”:false,”csslayout”:””,”title”:”Amount for childrenu2019s education”,”predefined”:””,”predefinedClick”:false,”required”:false,”readonly”:false,”size”:”small”,”currencySymbol”:”$”,”currencyText”:””,”thousandSeparator”:”,”,”centSeparator”:”.”,”noCents”:false,”min”:””,”max”:””,”formatDynamically”:true,”fBuild”:{},”parent”:””},{“form_identifier”:””,”name”:”fieldname6″,”shortlabel”:””,”index”:4,”ftype”:”fcurrency”,”userhelp”:”Optional. Add an amount here if you want your life insurance to pay off existing debts, such as a mortgage, in a lump sum.”,”userhelpTooltip”:false,”csslayout”:””,”title”:”Amount for paying off debt”,”predefined”:””,”predefinedClick”:false,”required”:false,”readonly”:false,”size”:”small”,”currencySymbol”:”$”,”currencyText”:””,”thousandSeparator”:”,”,”centSeparator”:”.”,”noCents”:false,”min”:””,”max”:””,”formatDynamically”:true,”fBuild”:{},”parent”:””},{“form_identifier”:””,”name”:”fieldname7″,”shortlabel”:””,”index”:5,”ftype”:”fcurrency”,”userhelp”:”Optional. Add an amount here if you want your life insurance to pay off existing debts, such as a mortgage, in a lump sum.”,”userhelpTooltip”:false,”csslayout”:””,”title”:”Existing life insurance”,”predefined”:””,”predefinedClick”:false,”required”:false,”readonly”:false,”size”:”small”,”currencySymbol”:”$”,”currencyText”:””,”thousandSeparator”:”,”,”centSeparator”:”.”,”noCents”:false,”min”:””,”max”:””,”formatDynamically”:true,”fBuild”:{},”parent”:””},{“form_identifier”:””,”name”:”fieldname8″,”shortlabel”:””,”index”:6,”ftype”:”fButton”,”userhelp”:””,”userhelpTooltip”:false,”csslayout”:””,”sType”:”calculate”,”sValue”:”Calculate”,”sOnclick”:””,”sLoading”:false,”fBuild”:{},”parent”:””},{“form_identifier”:””,”name”:”separator1″,”shortlabel”:””,”index”:7,”ftype”:”fSectionBreak”,”userhelp”:””,”userhelpTooltip”:false,”csslayout”:””,”title”:””,”fBuild”:{},”parent”:””},{“dependencies”:[{“rule”:”valueu003E1″,”complex”:false,”fields”:[“fieldname1″,”fieldname9″,”fieldname10″,”fieldname11″,”fieldname12″]}],”form_identifier”:””,”name”:”fieldname14″,”shortlabel”:””,”index”:8,”ftype”:”fCalculated”,”userhelp”:””,”userhelpTooltip”:false,”csslayout”:””,”title”:”Hidden – Show Results”,”predefined”:””,”required”:false,”size”:”medium”,”eq”:”fieldname3*0.7*fieldname13″,”suffix”:””,”prefix”:””,”decimalsymbol”:”.”,”groupingsymbol”:””,”readonly”:true,”hidefield”:true,”fBuild”:{},”parent”:””},{“dependencies”:[{“rule”:””,”complex”:false,”fields”:[“”]}],”form_identifier”:””,”name”:”fieldname1″,”shortlabel”:””,”index”:9,”ftype”:”fCalculated”,”userhelp”:””,”userhelpTooltip”:false,”csslayout”:””,”title”:”After-tax income to replace”,”predefined”:””,”required”:false,”size”:”medium”,”eq”:”PREC(fieldname3*0.7*fieldname13, 2)”,”suffix”:””,”prefix”:”$”,”decimalsymbol”:”.”,”groupingsymbol”:”,”,”readonly”:true,”hidefield”:false,”fBuild”:{},”parent”:””},{“dependencies”:[{“rule”:””,”complex”:false,”fields”:[“”]}],”form_identifier”:””,”name”:”fieldname9″,”shortlabel”:””,”index”:10,”ftype”:”fCalculated”,”userhelp”:””,”userhelpTooltip”:false,”csslayout”:””,”title”:”Optional coverage (debt & education)”,”predefined”:””,”required”:false,”size”:”medium”,”eq”:”PREC(fieldname5+fieldname6, 2)”,”suffix”:””,”prefix”:”$”,”decimalsymbol”:”.”,”groupingsymbol”:”,”,”readonly”:true,”hidefield”:false,”fBuild”:{},”parent”:””},{“dependencies”:[{“rule”:””,”complex”:false,”fields”:[“”]}],”form_identifier”:””,”name”:”fieldname10″,”shortlabel”:””,”index”:11,”ftype”:”fCalculated”,”userhelp”:””,”userhelpTooltip”:false,”csslayout”:””,”title”:”Total coverage needed”,”predefined”:””,”required”:false,”size”:”medium”,”eq”:”PREC(fieldname1+fieldname9, 2)”,”suffix”:””,”prefix”:”$”,”decimalsymbol”:”.”,”groupingsymbol”:”,”,”readonly”:true,”hidefield”:false,”fBuild”:{},”parent”:””},{“dependencies”:[{“rule”:””,”complex”:false,”fields”:[“”]}],”form_identifier”:””,”name”:”fieldname11″,”shortlabel”:””,”index”:12,”ftype”:”fCalculated”,”userhelp”:””,”userhelpTooltip”:false,”csslayout”:””,”title”:”Existing coverage (assets & insurance)”,”predefined”:””,”required”:false,”size”:”medium”,”eq”:”PREC(fieldname4+fieldname7, 2)”,”suffix”:””,”prefix”:”$”,”decimalsymbol”:”.”,”groupingsymbol”:”,”,”readonly”:true,”hidefield”:false,”fBuild”:{},”parent”:””},{“dependencies”:[{“rule”:””,”complex”:false,”fields”:[“”]}],”form_identifier”:””,”name”:”fieldname12″,”shortlabel”:””,”index”:13,”ftype”:”fCalculated”,”userhelp”:””,”userhelpTooltip”:false,”csslayout”:””,”title”:”New life insurance needed”,”predefined”:””,”required”:false,”size”:”medium”,”eq”:”PREC(fieldname10-fieldname11, 2)”,”suffix”:””,”prefix”:”$”,”decimalsymbol”:”.”,”groupingsymbol”:”,”,”readonly”:true,”hidefield”:false,”fBuild”:{},”parent”:””}],{“0”:{“title”:”Life Insurance Calculator”,”description”:””,”formlayout”:”top_aligned”,”autocomplete”:0,”formtemplate”:””,”evalequations”:0,”evalequationsevent”:2,”persistence”:0,”customstyles”:””},”formid”:”cp_calculatedfieldsf_pform_1″}]; Choosing A Million Dollar Insurance Policy According to Policy Genius, the average cost for a 20-year $1 million term life insurance policy for a 35-year-old male is $53 per month. However, your rate will vary according to the following factors. Factors that affect your rate: Your age Your health Your gender Your hobbies Your coverage amount and policy term Where to start? The best, and easiest place to start is online. I recommend having two or three insurers compete for your business to make sure you get the best rate and coverage. To see how cheap term life can be, choose your state from the map above to be matched with top life insurance providers instantly. Factors That Affect How Much You Need Let’s look at the individual components that can quickly add up to over a million-dollar policy. Income Replacement This is where things can get a bit intimidating. Even if you earn a modest income, you may need close to $1 million to replace that income after your death in order to provide for your family’s basic living expenses. The conventional wisdom in the insurance industry is that you should maintain a life insurance policy equal to between 10 times and 20 times your annual income. So if you earn around $50K per year, that would mean policy coverage between $500K and $1 million. The complication today is that with interest rates being as low as they are that might not be enough either. For example, if you have a $1 million policy that could be invested at 5% per year, your family could live on the interest earned – which conveniently comes to $50,000 per year – for the next 20 years. That would still leave the original $1 million intact to cover other expenses. But with today’s microscopic interest rates, there’s no way to get a guaranteed return of 5% on your money, certainly not for 15 or 20 years. That brings us back to simple math – multiplying your annual