Tech firms ask U.S. Supreme Court to block Texas social media law

[ad_1] Tech firms ask U.S. Supreme Court to block Texas social media law [ad_2] Source link

Tech firms ask U.S. Supreme Court to block Texas social media law Read More »

[ad_1] Tech firms ask U.S. Supreme Court to block Texas social media law [ad_2] Source link

Tech firms ask U.S. Supreme Court to block Texas social media law Read More »

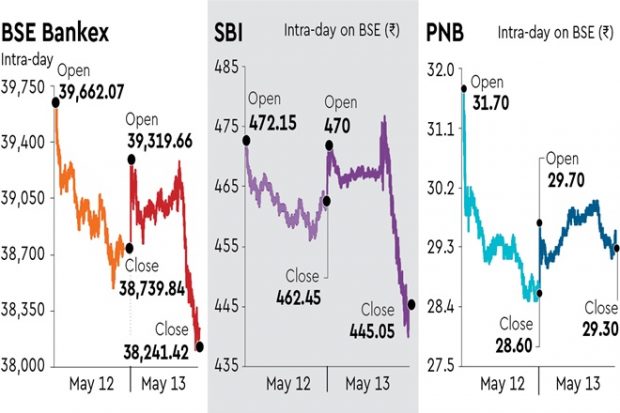

[ad_1] After plummeting 1,255 points on Thursday, the BSE Bankex lost further ground on Friday as it fell 498 points, wiping out a total market capitalisation to the tune of Rs 1.1 trillion. The slide on Friday began after State Bank of India (SBI)’s net profit of Rs 9.113.53 crore for Q4FY22 missed Bloomberg estimates of Rs 10,180 crore. The net interest margin saw only a slight sequential increase. While the lender’s slippages rose to Rs 2,845 crore from Rs 2,334 crore in the December 2021 quarter, the gross non-performing asset (NPA) ratio narrowed 53 bps sequentially to 3.97% and the net NPA ratio declined 32 bps to 1.02%. However, it set aside Rs 3,260 crore as bad loan provisions, around 5% higher than the quantum in the December 2021 quarter. The stock ended the session lower by 3.8% at Rs 445.05. The sentiment in banking stocks had already been hit on Thursday after Punjab National Bank (PNB) reported a poor set of earnings with a 65% y-o-y drop in net profits due to a 35% increase in credit costs. The slippages jumped sharply to around 6% annualised, meaningfully outpacing recoveries. The net interest income (NIM) was up by a muted 5% y-o-y. The stock crashed to Rs 28.60 at close on Thursday from the previous close of Rs 33.1. While loan growth has been reasonably good at most state-owned lenders, some have reported bigger slippages and made higher loan loss provisions suggesting the balance sheets, although much stronger, are not fully cleaned up yet. There is some concern among analysts that rising interest rates – given a big chunk of loans is linked to the repo rate – could stymie demand for credit. While Bank of Baroda (BoB) saw a turnaround with net profits for the March quarter coming in at Rs 1,779 crore against a loss of Rs 1,047 crore in Q4FY21, these were supported by tax benefits. The lender on Friday reported a good increase in the net interest income of 21% y-o-y though there was a sequential decline in the NIM of around seven bps. Other income was down 72% y-o-y. Ahead of the results, the stock closed lower by 1.1% at Rs 95. Again, Union Bank of India on Friday reported an 8.3% y-o-y rise in net profits to Rs 1,440 crore on the back of a strong 25% growth in NII to Rs 6,769 crore.The value of slippages in the March quarter was Rs 5,672 crore, higher than Rs 3,411 crore in the December 2021 quarter. Provisions fell 2% y-o-y to Rs 3,618 crore. However, margins were under pressure and fell 25 bps sequentially to 2.75% in Q4FY22. Asset quality improved as the gross NPAs as a share of total advances fell 51 bps on a sequential basis to 11.11% and the net NPA ratio declined 41 bps to 3.68%. Last week, Canara Bank (CBK) reported a mixed operating performance with NII growing 25% y-o-y and fresh slippages at an elevated Rs 4,740 crore. The lender’s net interest margin expanded by 10 bps sequentially to 2.9%. Healthy recoveries, upgrades and write-offs helped the bank announce better asset quality. The GNPA ratio improved by 29 bps q-o-q to 7.51%, while the net npa was better by 21 bps at 2.65%. [ad_2] Source link

Modest earnings and missed estimates: SBI numbers singe BSE Bankex Read More »

[ad_1] If you love Crocs, don’t miss these hot deals! For a limited time, Crocs is offering up to 50% off clogs and sandals for the family! Even better, you can get an additional 20% off 2 pairs, 30% off 3 pairs, or 40% off 4 pairs when you use the promo code SAVEMORE at checkout! Or, get $15 off $75 orders with promo code SAVE15 at checkout, or $20 off $100 orders when you use the promo code SAVE20 at checkout. Please note that only one code can be used per order. Here are some deals you can get… Get these Classic Crocs Glitter Sandals for just $20.25 (regularly $39.99)! Choose from two colors. Get these Classic Crocs Out of this World Sandals for just $20.25 (regularly $39.99)! Get these Kids’ Classic Out of this World II Clogs for just $25 (regularly $39.99)! Choose from three colors. Get these Classic Lined Bleach Dye Clogs for just $38.99 (regularly $64.99)! Get these Kids’ Baya Clogs for just $29.99 (regularly $39.99)! Choose from six colors. Shop the entire sale here. Shipping is free on orders over $44.99. Thanks, Hip2Save! [ad_2] Source link

HOT Deals on Crocs for the Family! Read More »

[ad_1] Texas grid operator calls for power conservation as temperatures climb [ad_2] Source link

Texas grid operator calls for power conservation as temperatures climb Read More »

[ad_1] S&P Global Ratings has revised the outlook on Tata Steel to ‘positive’ from ‘stable’ on the back of continuing strong cash flows, while reaffirming its ‘BBB-‘ rating. The Tata Group company is expected to generate substantial free operating cash flows over the next two years owing to continuing strong steel prices. The resilience of the company’s credit metrics to steel price cycles has also strengthened following a significant reduction in debt over the past 18 months. S&P estimates Tata Steel’s adjusted debt-to-Ebitda (earnings before interest, tax, depreciation, and amortisation) ratio to stay below 2.5x at the bottom of the cycle. “We are therefore revising our rating outlook on TataSteel and its subsidiary ABJA Investment Co. Pte. Ltd. to positive from stable. At the same time, we are affirming our ‘BBB-‘ long-term issuer credit ratings on the two companies and the ‘BBB-‘ long-term issue rating on the senior unsecured notes that ABJA issued,” the ratings firm said in a note on Friday. The positive outlook reflects the potential for an upgrade for TataSteel over the next 12-24 months if the company continues to reduce leverage and improves its resilience to steel price cycles, it said. Tata Steel’s strong free operating cash flows over the next two years will strengthen its credit profile. It is estimated that the company will generate $3-4 billion of free operating cash flows annually over the next two years, given continued strength in steel prices. “This is based on our estimate of Ebitda/ tonne for the Indian operations averaging about Rs 20,000 over the next two years. This is about 40% higher than typical levels in the past,” the S&P note said. Cash flows will also aid in further debt reduction in the absence of increased investments or shareholder returns. Tata Steel intends to increase its capacity in India to 40 million tonne by 2030 from about 25 million tonne at the end of FY24. The company has indicated that it could accelerate some capital expenditure given current conditions in the steel industry. “Even in such a scenario, we believe Tata Steel’s credit metrics will strengthen, though the pace of deleveraging may be slower than in the past 18 months. Besides, the increase in scale without material incremental debt will enhance the company’s credit profile in the longer term,” it said. Tata Steel’s adjusted debt as of March 31, 2022, is down by close to 45% from about Rs 1.1 trillion a year earlier. The reduced debt and the positive operating outlook should keep its ratio of funds from operations to debt above 75% over the next two years. At the normal level of steel prices, it is estimated that the company’s Ebitda per tonne will be about Rs 14,000 per tonne, compared with Rs 19,000- Rs 23,000 per tonne in S&P’s base case. The company has deleveraged sharply over a short period, with an adjusted debt-to-Ebitda ratio of 1x as of March 31, 2022, compared with about 6.6x as of March 31, 2020. “We expect Tata Steel’s credit metrics to be above our upgrade trigger even if steel prices normalise over the next two years. However, the cushion remains limited against unforeseen debt-funded investments and steel price downturns. Therefore, the company’s continued commitment to operate at a lower leverage would be key to a higher rating,” it said. [ad_2] Source link

S&P revises outlook on Tata Steel to ‘positive’ from ‘stable’ Read More »

[ad_1] When the markets are in turmoil and inflation is increasing, investors become very concerned about their money. Interest rates are creeping up but the national average on savings accounts is still around 0.5%. Where is an investor supposed to park their money and make a decent return without a ton of risk? One surprising answer is the U.S. government. Let me explain. Through TreasuryDirect.gov investors can purchase I bonds. Series I bonds are currently yielding 7.12% and they’re low risk. But that rate is set to increase on July 1st to 9.62%. It doesn’t get much better than that at this point, especially when you look at how little high yield savings accounts and CDs are offering right now. No wonder I bonds have gotten a lot sexier lately. The “I” in I bonds stands for “inflation-linked”. Series I bonds are government savings bonds whose return increases with inflation made exactly for these times as an additional bonus. They’re easy to purchase and you can even buy one by the time you get done reading this article. By the end of this article on Series I Bonds you’ll: You’ll know whether a Series I Bond might be right for you How to buy a Series I Bond (step by step) Some important restrictions or catches of buying an I Bond Should You Buy I Bonds For Your Portfolio? These two questions will help you figure out if an I bond might be right for you: Do you have extra cash above and beyond what you need in your emergency fund? Is it possible that you might still need this extra cash say next year, in two years, or perhaps even five years? For example, if you’re saving up for a house, a wedding, or a teen that’ll be going to college soon, or maybe your retirement in the near future then YES, a Series I Bond is something you should consider to inflation-proof your extra cash at the moment. You can also consider I Bonds if you’re looking for better banking alternatives in 2022. How Safe Are Series I Bonds? As I mentioned earlier, I Bonds are U.S. government savings bonds that help protect you during inflationary times on the most basic level. Think of it as a loan that you give to the US government alone, whose interest rate is adjusted upward or downward based on where inflation is because I Bonds are backed by the US government. They are low-risk, safe investments that pay a high return. What About Default Risk? With Series I Bonds, investors may be concerned about “credit risk”. The U.S. government will not default on your I Bond or refuse to pay back your money when you redeem it a year later, this safety has, however, historically come at a price. Typically in times of low inflation, I Bonds will pay lower returns compared to other types of bonds such as municipal bonds or high yield bonds. It wasn’t until recently that the yield on Series I Bonds caught the interest of investors paying a salty 7.12%. But when the Fed increased interest rates the CPI also adjusted so now I Bonds will be paying 9.62%. Think about that: Earning 9.62% GUARANTEED. Non-Marketable Securities Series I Bonds have a 30-year term and can only be purchased directly from the US Treasury. This means they’re non-marketable (not available in the secondary market). You can’t purchase these at your local brokerage firm or in your retirement account. They are also not available on your favorite online broker or even investment apps. So no Fidelity, Vanguard, Betterment, Robinhood, etc. Now some folks will say that this is a disadvantage and it is an extra step, but this extra step takes literally five minutes. But five minutes to make a 9.62% return is totally worth it! How To Buy A Series I Bond (Step by Step) What you need to do first is to go to the US treasury website, TreasuryDirect.gov, and open an account, assuming you don’t have one already. Then click on “TreasuryDirect” under the Individual/Personal tab. What’s going to pop up next is this page showing you the three-step process for setting up an account. Step one: Choose the Type of Account There are several different types of accounts you can open to purchase Series I Bonds. Most investors will select the “Individual Account” option. In addition to that option, you can also select “Entity Account” if you meet those requirements. Types of Entity Accounts for Business or Organization: Corporation Partnership Limited Liability Company (LLC) Professional Limited Liability Company (PLLC) Sole Proprietorship Types of Entity Accounts for Estates or Trusts: Deceased Estate Living Estate Trust Step 2: Personal Information and Banking Step two will require you to input your personal and banking information. You’ll have to fill out some basic personal and banking information. You’ll need to provide your name, social security number or tax ID number, driver’s license information address, at least one phone number, email, and bank account information, everything that is marked where the red asterisk is required. This bank account should be the one that you’re using to fund your I Bond purchase with a triple quadruple check that your banking information is correct because changing it will take a fair bit of paperwork and legwork. Now read through this section, check this box to certify your social security or tax ID number then click submit. This will take you to the next screen where you should double-check all your personal information and banking details. Scroll down and submit if correct, or go back and edit. If there are any mistakes, once you click submit, this will be the screen you see next, choose an image and an image caption. And after this, choose your password, password reminder, and three security questions. Step 3: Make Your Treasury Account Secure Step three is setting up your password, password reminder, and security questions. Scroll down and click on apply now. After selecting the type of account you are opening then

How to Buy Series I Bonds at 9.62%: Step by Step Tutorial Read More »

[ad_1] Running low on trash bags? Here’s a great stock up deal! Amazon has these Glad ForceFlex Tall Kitchen Drawstring Trash Bags, 13 Gallon, Unscented, 120 Count for just $14.63 shipped when you clip the $3 off e-coupon and checkout through Subscribe & Save! This is a great stock up deal. Note: Once your order ships, you can go into your Amazon account and cancel your subscription if you don’t want recurring orders. [ad_2] Source link

[ad_1] SEC sues Florida firm that raised $410 million for IPO-linked fraud -filings [ad_2] Source link

SEC sues Florida firm that raised $410 million for IPO-linked fraud -filings Read More »

[ad_1] State-owned Bank of Baroda Friday reported a standalone profit after tax of Rs 1,779 crore in the quarter ended March 2022, helped by higher interest income and fall in bad loans. The lender had a loss of Rs 1,047 crore in the year-ago period. In the last financial year, the bank posted a standalone net profit of Rs 7,272 crore compared to Rs 829 crore in 2020-21. “The year went as per the guidance we gave at the beginning of the year. Our thought was that we should grow as per market and also protect our margins because liquidity was abundant and corporate lending was under pressure in terms of pricing. “We have grown our (global gross) loan book by about 8.9 per cent during the year,” the bank’s Managing Director and CEO Sanjiv Chadha said. On the liability side, he said the bank wanted to make sure its deposit growth remained in line with asset growth so that there was no overhang of liquidity. “So by keeping that discipline, we were able to have our CD (Credit Deposit) ratio at two percentage points higher at the end of the year as compared to the beginning of the year. On the deposit side, the growth came from the Casa ratio which moved to 44 per cent,” he said. Net Interest Income (NII) registered a growth of 21.2 per cent at Rs 8,612 crore in the fourth quarter of FY22 as against Rs 7,107 crore in the year-ago period. Net Interest Margin (NIM) in the fourth quarter stood at 3.08 per cent, an increase of 36 bps compared to the same quarter of FY21. Net Interest Margins (NIM) improved by 32 basis points (bps) y-o-y to 3.03 per cent in FY22. Gross Non-Performing Assets (NPAs) reduced to Rs 54,059 crore in the latest quarter from Rs 66,671 crore in the year-ago period. Gross NPA ratio improved to 6.61 per cent from 8.87 per cent. The net NPA ratio improved to 1.72 per cent as compared with 3.09 per cent. Slippages for the year were contained at 1.61 per cent. “We have been guiding that there is a secular trend of improvement in corporate credit quality. This is something that we have seen sustained over the last one year despite the impact of COVID and we expect it to continue. “So, it should mean that slippage should come down further. We should see a further moderation in terms of credit cost. GNPA, net NPA have come down almost every quarter for the last year and we should see further improvement this year also,” Chadha said. Fresh slippages stood at Rs 4,514 crore in the reporting quarter. It recovered Rs 2,136 crore of bad loans and upgraded Rs 1,112 crore of NPAs during the quarter. Provision coverage ratio stood at 88.71 per cent including technical write off accounts and 75.28 per cent excluding TWO accounts in Q4FY22. Total provisions increased by 5.1 per cent to Rs 3,736 crore as against Rs 3,555 crore in the same quarter of the previous fiscal. Provisions for bad loans rose by 13.2 per cent to Rs 5,200 crore from Rs 4,593 crore. Capital to Risk (Weighted) Assets Ratio (CRAR) improved to 15.98 per cent in March 2022 from 14.99 per cent in March 2021. Tier-I stood at 13.49 per cent (Common Equity Tier-1 at 11.74 per cent, Additional Tier 1 at 1.75 per cent) and Tier-II stood at 2.49 per cent as of March 2022. The lender will look at raising Rs 2,000-2,500 crore through issuance of additional tier 1 bonds this year, Chadha said. Domestic advances of the bank increased by 6.7 per cent to Rs 6,84,153 crore as on March 31, 2022 from Rs 6,41,076 crore as of March 31, 2021. Retail loan portfolio grew by 16.8 per cent led by growth in personal loan portfolio by 108.1 per cent, auto loan by 19.5 per cent and education loan by 16.7 per cent on a y-o-y basis. Agriculture loan portfolio grew by 10.3 per cent y-o-y to Rs 1,09,796 crore and MSME portfolio increased by 5.4 per cent y-o-y to Rs 96,863 crore. Corporate advances rose by 3.1 per cent to Rs 3,00,693 crore as of March 31, 2022. Chadha expects a healthy growth in corporate loan book in the current fiscal. “We were committed not to dilute our margins so we made sure that we focus on areas where margins are better. I expect that with RBI moving to normalising interest rates, it should be possible to both grow as well as keep margins intact. I would expect corporate loan growth to be better this year,” he said. The lender is expecting a loan growth of 10-12 per cent in FY2023, he said. According to him, it may go for listing of its life insurance joint venture — IndiaFirst Life Insurance — where it holds 65 per cent stake, in the current financial year. The bank’s scrip ended at Rs 94.95 apiece, down 1.15 per cent on BSE. [ad_2] Source link

Bank of Baroda posts Rs 1,779 crore profit in March quarter Read More »

[ad_1] Million Dollar Journey editor and Canadian Financial Summit founder Kyle Prevost shares financial headlines and offers context for Canadian investors. Making sense of the nonsensical I’m one month into writing “Making sense of the markets” when this happens: everything and anything. Is there like a dollar sign-shaped bat signal we can use to summon Dale Roberts back? (Roberts is the original writer of this column.) Making sense of the short-term movements in asset markets is never exactly easy. But for the last two years, forecasting most of the world’s stock markets has meant deciding which beautiful sky was the sunniest. We had it pretty good. Recent headlines, though, have proven that the outlook just got a lot cloudier. The first thing to keep in mind when looking at the stock market’s serpentine moves over the last week is that prices really are pretty rational in the long term. Over the short-term, however—not so much. How do we justify a stock price dropping 10% or more of the price evaluation before its earnings announcement, despite meeting earnings expectations for the last three months? The lesson being, of course, that while markets are generally efficient, it can take them a while to realize that efficient pricing mechanism’s full potential. If stock prices aren’t responding to the fundamentals, such as earnings, then why are they going down so fast? Well, it’s probably a combination of many things. And they’re probably not particularly relevant in the long run. Here are some of the plausible theories I believe are impacting investor sentiment. Rising interest rates make safer investments more attractive. If you can find a five-year guaranteed investment certificate (GIC) for 4.15%, suddenly those dividend stocks don’t look quite so unbeatable right? Rising interest rates make equity in indebted companies much less attractive. When central banks were begging for business to borrow money and throw it at the economy, no one was bothered much by huge loans used to fuel growth. It turns out that when a bigger and bigger percentage of a company’s revenues go towards paying interest, shareholders don’t get as much put in their collective pocket. New-age algorithmic trading combined with traditional investor panic can quickly build downward momentum that isn’t really justified by anything other than it’s physiologically really difficult to see the value of your portfolio go down. Investors have become more and more comfortable with borrowing money in order to invest in stocks, or to speculate on stock movements using options. This is referred to as “leverage.” And when asset prices are going up, it allows you to make money using other people’s money—which is a pretty good deal. The problem: Just as leverage can accelerate the good times, it can also hit the gas on the bad times. As lenders see asset valuations drop, they worry about defaulted loans, and they force leveraged investors to sell via a demand called a “margin call.” If the bank gets worried that you won’t be able to pay your loan, they will force you to sell the assets you currently have. Of course, the more people are forced to sell, the lower the prices go. And the cycle can quickly become supercharged. Even with the above four points, there comes a point when an honest market commentator has to simply throw up their hands to say, “I don’t know. It’s just weird right now, and I don’t really get it.” I admit that it’s not the sort of bold pronouncement that TV financial gurus love to make. But what else is there to do after the following sequence of events: The U.S. Federal Reserve (a.k.a. “the Fed”) decides to implement the exact 0.50% interest rate increase it forecasted. The chairman of The Fed says he was just kidding about a more aggressive 0.75% rate hike. Stock prices go up. Experts say this is because investors were afraid of the more aggressive hike, which is now off the table. The next day, without anything new and noteworthy happening, stocks plummet. If nothing else, we can safely say that inflation has decisively captured the attention of both the general public and the markets (as evidenced by this Amazon find). Amazon.co.uk screenshot courtesy of Kyle Prevost. And, how’s this for a head-scratcher? On top of all this, it seems there are more jobs than people who want one! Sometimes the markets just don’t want to be made sense of. Is the shine off Shopify? Once upon a time, back in 2020, Shopify (SHOP) was Canada’s little tech company that could. It even managed to briefly top the banks, and mining and energy companies to become the largest company on the Toronto Stock Exchange (as measured by market capitalization). Since then, things haven’t exactly stayed on track. Source: Financial Times With shares down more than 70% YTD, SHOP has many investors wondering what it did to deserve such a drastic penalty. As I wrote last week, the problem with tech company stocks at the moment isn’t necessarily the underlying companies or their ability to earn a lot of revenue. The issue is that investors have paid ever-increasing premium prices for these shares because they anticipated revenue and earnings would continue to grow at unprecedented rates. The math isn’t quite the same as owning a utility stock, like Fortis (F), where a conservative growth rate is almost locked in for the long term. So, when SHOP announced its adjusted earnings per share was only $0.20—when analysts predicted $0.65—it shook investor confidence at a time when overall sentiment was already in freefall in regards to tech stocks. That said, this is the same company that is growing revenues pretty darn quickly! SHOP reported, even as many retail customers were moving back to in-person versus online shopping, that their revenue went up 21.4%, to 1.2 billion. Source: Reuters While it is logical that the company’s value would drop after revealing its profits weren’t growing as quickly as shareholders had hoped, this brutal correction seems a bit

Making sense of the markets this week: May 15 Read More »