Republican lawmaker urges top Senate Democrat to give gun talks time

[ad_1] Republican lawmaker urges top Senate Democrat to give gun talks time [ad_2] Source link

Republican lawmaker urges top Senate Democrat to give gun talks time Read More »

[ad_1] Republican lawmaker urges top Senate Democrat to give gun talks time [ad_2] Source link

Republican lawmaker urges top Senate Democrat to give gun talks time Read More »

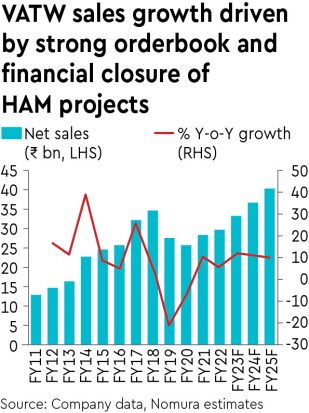

[ad_1] Q4FY22 sales were at Rs 8.91 bn (down 11% y-o-y, missed our estimate by 9%) highlighting a slowdown in execution in overseas order. The weaker execution also led to a miss on EBITDA margin by 110bp at 8% despite stable gross margins. Weak order inflows at Rs 36.5 bn was disappointing; policy of selective bidding, while appreciated, leading to weak growth: Management has guided for double-digit sales and order inflow growth in the near term. However, a policy of selective bidding focused on technologically complex tenders in the international market may lead to order inflows remaining in the Rs 30-35 bn range over FY23-25F. However, if VATW secures the large `60-bn Chennai desalination tender, then we would expect significant upside to our sales estimates. Sales momentum may be weak in H1FY23F due to lack of contribution from Russian order: Russia accounted for Rs 11 bn of the Rs 89.8-bn orderbook and since the start of Russia-Ukraine conflict progress has stopped due to payment mechanism issues (NB: no cash collection is pending). The prevailing US and EU sanctions may make progress on this order challenging, which could impact near-term sales growth. Management expects sales to pick up in the Middle East and compensate in FY23. Cash collections robust in FY22, gross margins strong despite commodity increase; remained net cash: Gross margin was stable at 23% for H2FY22 despite a sharp rise in commodity prices, which is a key positive. We estimate that with a revival in execution EBITDA margin for FY23-25F could be sustained in the 8-9% range. The orderbook is 95% funded by central government or multi-lateral agencies, and this is reflected in robust cash collections in Q4FY22. Current receivables remained flattish in absolute terms despite sales growth of 7% in FY22. Trading at 8.2x FY24F EPS of Rs 29.8; maintain Buy with TP of Rs 448 We cut FY23/24F EPS by 31%/29% to factor in impact of stalled execution in Russia and slow pace of order wins in FY22. We value VATW at 14x (based on sustainable ROE of 11%) FY24F EPS of Rs 29.8 rolled forward to Jun-23 to arrive at our TP of Rs 448, implying >80% upside, and reiterate Buy rating. Key risks include slowing domestic capex for water. [ad_2] Source link

A Tech Wabag Rating: Buy | Slower execution cast a shadow on Q4FY22 Read More »

[ad_1] It’s a tough time for mortgage lenders. A rapid rise in mortgage rates and a big drop in origination volume has led to thousands of industry job losses over the last six months. And it’s likely to continue – executives are calling this one of the most challenging periods in memory. By some estimates, origination volume will fall in 2022 to about $2 trillion, about half the volume from the record-breaking years of 2021 and 2020. Few originators have been left unscathed by the industry-wide reduction in capacity. Wells Fargo, one of the nation’s largest banks, had at least 114 layoffs in its home lending business following a drop in revenue in that division in the first quarter of 2022. Sources told HousingWire the number was substantially higher, though the lender declined to provide figures. Nonbank lenders such as Pennymac, Mr. Cooper, loanDepot, Guaranteed Rate, Fairway Independent Mortgage, Interfirst Mortgage Co., Movement Mortgage and Better.com all conducted at least one round of workforce reductions this year as mortgage rates surged past the 5% mark. Below is a roundup of some of the notable lenders that have issued pink slips this year. We have undoubtedly missed some job cuts; you can share news of layoffs anonymously by emailing Connie Kim at connie@hwmedia.com. This list will be updated throughout the year. Wells Fargo: at least 114 employees in home lending Wells Fargo, the third-biggest lender by volume in 2021, laid off at least 114 employees in its home lending division this year. As of May 27, Iowa Workforce Development lists 49 layoffs at the Wells Fargo campuses in Des Moines and 34 employee reductions in West Des Moine. Impacted employees, all in the home lending division, will receive pink slips in June and July, according to Iowa’s WARN notification list. According to Worker Adjustment and Retraining Notification (WARN) notices submitted to the California Employment Development Department (EDD) earlier this month, the company plans to cut 31 jobs in the home lending business, in letters to the EDD reviewed by HousingWire. Layoffs included 17 associate loan servicing representatives and eight loan servicing representatives as well as senior operations processors and senior loan servicing representatives. “The home lending displacements are the result of cyclical changes in the broader home lending environment,” Lylah Holmes, a spokesperson at Wells Fargo, told HousingWire. Wells Fargo will be providing severance and career counseling, and helping affected employees identify other positions within the bank. The bank’s revenues in the home lending business totaled $1.5 billion in the first quarter this year, a 19% drop compared to the previous quarter and 33% lower than the same period in 2021. Wells Fargo executives in early June said the bank was considering pulling back on its mortgage business, where, beyond the challenges related to a decline in originations, it has also struggled with scandals related to minority lending. loanDepot: Unknown loanDepot, the fourth-largest lender, per mortgage data firm Polygon Research, conducted an unspecified number of layoffs in late May. Multiple sources told HousingWire that “hundreds” were let go. Jonathan Fine, loanDepot’s vice president of public relations, declined to say how many positions were cut and suggested that a review of the earnings call transcript from the first quarter would provide needed information. In April, loanDepot announced plans for potential layoffs in the company’s first quarter earnings call after reporting a net loss of $91.3 million. Company chief financial officer Patrick Flangagan said loanDepot doesn’t expect to be profitable this year and shared plans to reduce marketing personnel expenses. Loan origination volume dropped 26% to $21.6 billion from the previous quarter, according to the firm, bringing the company’s market share down to 3.1%. The lender expects loan origination volume to post between $13 billion and $18 billion in the second quarter of this year. Company executives said loanDepot is not expected to be profitable in 2022. NewRez LLC: 386 employees New Residential Investment Corp., the sixth-largest lender per Polygon Research, eliminated 386 positions, accounting for about 3% of the mortgage division’s workforce, in February. The layoff decision followed New Residential Investment Corp.’s acquisition of multichannel lender Caliber Home Loans last year. “As we continue to create synergies between companies, we are creating a structure to streamline business channels and create long-term growth,” the NewRez spokesperson wrote in an email to HousingWire in February. Caliber was a heavy-hitter across multiple origination channels, generating $80 billion in originations and $153 billion in servicing in 2020. Best known for its distributed retail footprint and its fair amount of business in correspondent and wholesale channels, NewRez/Caliber had 3.7% of market share in 2021, according to data from Inside Mortgage Finance. Owning Group: 189 employees California-based Owning Corp., a direct-to-consumer lender acquired by Guaranteed Rate in February 2021, cut 189 jobs across three rounds from February to April. The layoffs included 51 mortgage specialists, the most heavily affected position, and 42 mortgage consultants. Employees that were let go also included underwriters, closers, and top executives such as lending directors and vice presidents for credit and underwriting. Owning is the second company acquired by Guaranteed Rate in 2021 to face layoffs in the challenging mortgage market this year. Early in January, Texas-based Stearns Lending, acquired in January 2021 from the financial giant Blackstone Group for an undisclosed sum, laid off 348 workers following the decision by Guaranteed Rate to discontinue operations of its third-party wholesale channel. Better.com: more than 4,000 workers Digital lender Better.com has already conducted three rounds of layoffs since late last year, and it’s unclear where the bottom is. The firm’s CEO infamously laid off 900 employees in a Zoom meeting in December where he then criticized the departing employees to remaining workers, 3,000 workers in March, some of which work in India, and an undisclosed number of people in April. The firm has been seeking to go public via a special purpose acquisition company (SPAC), known as Aurora Acquisition Corp. But without reliable access to purchase business, conditions look bleak for Better. An S-4 filing from

These mortgage lenders have cut jobs in 2022 Read More »

[ad_1] The post How to Buy Bonds appeared first on Millennial Money. One of the biggest mistakes that young investors make is they put all of their efforts into the stock market—investing only in individual stocks and funds. In addition to investing in the stock market, it’s also a good idea to purchase other types of financial instruments like bonds. Investing in the bond market is a great option for all types of investors, from people who are just starting, to people who have been managing personal finance for decades. Keep reading to learn the bond basics you need to make informed investments in the bond market. Table of contents What Is a Bond? The Benefits of Buying Bonds Diversification Less Risk for Investors High Interest The Disadvantages of Bonds Fixed Returns Inflation Less Liquidity How to Buy Bonds Use a Broker Treasury Direct Exchange-Traded Fund (ETF) Types of Bonds to Explore Treasury Bonds Treasury Bill (T-Bill) Treasury Note (T-Note) Treasury Inflation-Protected Securities (TIPS) Treasury Bonds Corporate Bonds Investment-Grade Bonds High-Yield Bonds Municipal Bonds General Obligation Bonds Revenue Bonds Conduit Bonds Tips for Buying Bonds Risk Tolerance Credit Rating Maturity Date Frequently Asked Questions (FAQs) What Is a Bond Fund? What Is an Exchange-Traded Fund? Are Bonds Riskier Than Stocks? What Is a New Issue? What Are Over-The-Counter (OTC) Bonds? Do You Have to Pay Federal Taxes on Muni Bonds? What Are Junk Bonds? Are Bonds Better Than Mutual Funds? How Does SIPC Protect Bondholders? The Bottom Line What Is a Bond? A bond is a fixed income debt instrument between a lender and a borrower. In short, a bond issuer takes money from a lender and agrees to pay it back with interest when the bond reaches maturity. The period of time until maturity can vary depending on the type of bond that is being issued. For example, some bonds reach maturity in one year while others can last 10 years or longer. The Benefits of Buying Bonds There are many reasons why investors should consider purchasing bonds. Here are a few of them. Diversification Bonds can add excellent diversification to a portfolio, offering investors a way to combat volatility during downturns. Bonds can provide steady and consistent returns with fixed interest payments. Less Risk for Investors Bonds are considered to be less risky for individual investors and riskier for companies. During bankruptcy events, bondholders have higher priority than shareholders for liquidation. So if a company goes under, bondholders are paid before common stock owners. Not bad! In addition, bonds are less volatile than stocks. Bond prices may change according to inflation and the overall economy. But they are more stable investments than stocks, which can significantly rise and fall in value. High Interest Another reason bonds are great is because they often have high interest rates. For example, high-yield corporate bonds have lower credit ratings and, as a result, they offer higher returns for investors. The Disadvantages of Bonds Fixed Returns On one hand, fixed interest rates offer more security. On the other, they can have diminished returns compared to equity investments. Investing too much of your portfolio in bonds may be too conservative for most early investors. Imagine locking into a low interest bond that matures in 10 years only to see interest rates rise significantly over the next few months. In such a scenario, you’re leaving money on the table. Inflation Not all bonds are protected from inflation. As such, long-term bonds can erode in value, leading to reduced returns for investors. Less Liquidity Bonds are not as easy to liquidate as stocks. Once you invest in a bond, your money is going to be locked up until it matures. While it’s possible to liquidate before maturity, you may have to pay penalties or sell at a lower rate. If you’re looking to invest in bonds but want liquidity, you may want to look into bond ETFs, which are traded like stocks. How to Buy Bonds Now that you have a general understanding of how bonds work, let’s explore how you can go about obtaining them. Use a Broker One way to buy bonds is to go through an online broker like Schwab, TD Ameritrade, or Fidelity. When you take this approach, you purchase bonds from other investors who are looking to sell them. Bonds are not listed on major exchanges. As such, investors must use brokers to arrange bond trades. Treasury Direct You can also purchase United States government bonds directly from the United States treasury via Treasury Direct. Purchasing government bonds directly can enable you to bypass brokers and agents, circumventing fees in the process. Exchange-Traded Fund (ETF) In addition to buying individual bonds, you can also purchase bond ETFs, which buy bonds from multiple companies. Funds may have a mix of short-, medium-, or long-term bonds. Learn More: Stocks vs. Bonds How to Protect Against Inflation on Your Financial Freedom Journey The Best Inflation-Proof Investments You Should Consider Buying Now Types of Bonds to Explore If you’re thinking about buying bonds, you need to determine which type of bond makes the most sense for your unique situation. Treasury Bonds The Department of the Treasury issues U.S. treasury bonds on behalf of the U.S. government. Since they are backed by the U.S. government, they are considered a very safe and secure investment. There are multiple types of treasury bonds available from the U.S. Treasury. Treasury Bill (T-Bill) T-Bills are short-term securities with varying term lengths. T-Bill maturity dates range from a few days to 52 weeks. Treasury Note (T-Note) T-Notes are longer-term securities that mature within 10 years. Treasury Inflation-Protected Securities (TIPS) TIPS are bonds and notes with principals that are adjusted based on the Consumer Price Index. These bonds pay interest every six months and mature in periods of five, 10, and 30 years. Treasury Bonds Treasury bonds also have longer maturity periods of around 30 years. These bonds pay interest every six months. Corporate Bonds Corporate bonds are debt securities issued

[ad_1] Don’t miss this great offer from Target! Through June 11th, Target is offering $10 off a $60+ purchase when you clip the Circle coupon here! This is a great way to save on groceries. [ad_2] Source link

Target Circle: $10 off a $60 purchase coupon Read More »

[ad_1] Russia sanctions U.S. treasury and energy secretaries, defence and media bosses [ad_2] Source link

Russia sanctions U.S. treasury and energy secretaries, defence and media bosses Read More »

[ad_1] Stock Market Rises After Weekly Loss The Wall Street Journal 5 things to know before the stock market opens Monday CNBC Consumer inflation data, Amazon stock split, Yellen testimony top week ahead Fox Business Early gains fade on Wall Street as trading remains choppy The Olympian What to watch today: Stocks set to bounce after Wall Street’s losing week CNBC View Full Coverage on Google News [ad_2]

Stock Market Rises After Weekly Loss – The Wall Street Journal Read More »

[ad_1] Finance minister Nirmala Sitharaman will on Tuesday launch a Single Nodal Agency (SNA) dashboard which will provide a platform for ministries/departments to monitor transfer of funds to states and their utilisation. In a statement the finance ministry said in order to give the stakeholders of SNA model the necessary feedback and monitoring tools in the operation of the schemes, Public Financial Management System (PFMS) has developed the SNA dashboard. “The dashboard depicts releases made to different states by ministries, further releases made by state treasuries to the SNA accounts, expenditure reported by the agencies, interest paid by banks to SNA accounts etc. in intelligible, informative and visually appealing graphics,” it said. “The SNA dashboard of PFMS will provide a platform for ministries/ departments to monitor their transfer of funds to states, its utilisation by the implementing agencies and assist in cash management of the government,” the ministry tweeted. The SNA dashboard forms part of public financial management reform that was initiated in 2021 with regards to the manner in which funds for Centrally Sponsored Schemes (CSS) are released, disbursed and monitored. “This revised procedure, now referred to as the SNA model, requires each state to identify and designate a SNA for every scheme. All funds for that state in a particular scheme will be credited in this bank account, and all expenses will be made by all other implementing agencies involved from this account,” the ministry said in a statement. The SNA model, therefore, ensures that allocation of funds to states for the CSS are made in a timely manner and after meeting various stipulations. “Effective implementation of this model has brought about greater efficiency in CSS fund utilisation, tracking of funds, pragmatic and just-in-time release of funds to the states; ultimately all contributing to better cash management of the government,” it added. The dashboard is being launched as part of the iconic week celebrations of Azadi Ka Amrit Mahotsav by the finance ministry. [ad_2] Source link

Nirmala Sitharaman to launch single nodal agency dashboard on June 7 Read More »

[ad_1] Over the next decade, the distinction between non-QM and QM loans will be blurred and the government-sponsored enterprises (GSEs) may have to accommodate the growing market of non-W2 borrowers. That is what mortgage executives and analysts forecasted for the non-QM market on Friday during IMN’s third annual Non-QM Forum in California as they took note of the rapidly expanding space and the revised Consumer Financial Protection Bureau (CFPB)’s General Qualified Mortgage final rule, better known as the QM rule. “One in three workers by the end of this decade will be on 1099s or running a small business,” said Nik Shah, chief executive officer at home,llc. “I think the need for bank statement mortgages, 1099 mortgages will grow exponentially. It could jump to 10, 20, 30% of the entire market share over the next decade.” S&P Global estimated non-QM volume reached $28.6 billion, about 0.7% of the overall mortgage market. This year, industry players such as Angel Oak Mortgage Solutions believe the non-QM market could grow as much as four-fold this year, with origination volume ranging between $70 billion and $100 billion. “If the non-QM borrowers become a third of the market, I’d more likely expect the agency footprint will change and grow,” said Chris Marazzo, a vice president at Citi. “They have the duty to serve to accommodate those borrowers.” Mortgage credit availability has remained low since the housing crisis in 2007. Since then, many lenders have been risk-averse and stuck to qualified mortgage originations as defined by the government-sponsored enterprises (GSEs), Fannie Mae, and Freddie Mac. With the non-QM market growing, GSEs are adapting to changing times. GSEs have been working to incorporate bank statements, which non-QM borrowers rely on as alternatives to payroll income, into their analysis for a long time, Marazzo noted. “(GSEs) opening the credit box, how do lenders, investors become more comfortable with affordability products that weren’t in the market before” are factors that are being closely watched, he added. “A lot of mortgage products are going to be QM,” said Pratik Gupta, head of collateralized loan obligation (CLO) and residential mortgage-backed securities (RMBS) Strategy at Bank of America Merrill Lynch, referring to the QM rule. “A lot of non-QM loans will meet this criteria,” Gupta added. The QM rule, which has a mandatory compliance date of October 2022, will remove the general QM loan debt-to-income (DTI) limit of 43% with a price-based approach that gives lenders relief for loans capped at 150 basis points above the prime rate. Regarding concerns about the Biden administration’s plan to close America’s housing supply shortfall, estimated at between 1.5 million units and 3.8 million units, depending on the source, Gupta raised concerns of potential oversupply of housing. “In terms of supply, the only thing that will crash the housing market is massive oversupply,” said Gupta. Gupta added: “Just increasing housing for the sake of housing supply will hurt the market. If demand drops, who is going to absorb the new units?” Earlier this month, the White House introduced the “Housing Supply Action Plan,” which aims to expand housing access for owners and renters through a combination of incentives, reforms, and financial mechanisms amid soaring inflation. Starting with the creation and preservation of affordable housing units in the next three years, the administration said the plan would “help close America’s housing supply shortfall in 5 years.” Analysts, including Logan Mohtashami, lead analyst for HousingWire, have brought up the need for improved housing inventory. In his recent commentary, Mohtashami noted that until the housing inventory is back up into a range of 1.52-1.92 million, the housing market will be “savagely unhealthy.” While the inventory of homes for sale in May rose 8% over the prior year – marking the first rebound in three years – the median national home price also climbed to an all-time high of $447,00, according to Realtor.com‘s monthly report. The post Do the GSEs need to start thinking about non-QM borrowers? appeared first on HousingWire. [ad_2] Source link

Do the GSEs need to start thinking about non-QM borrowers? Read More »

[ad_1] This Outdoor Market Patio Umbrella adds a cooling and colorful addition to every outdoor sitting area. You can get this highly-rated Outdoor 7.5ft Market Patio Umbrella with Push Button Tilt and Crank Lift for just $39.99 shipped when you use the promo code BCPSHADE at checkout! Choose from 10 color options. Note: You’ll also need the base that’s linked in the item description. Valid through June 12th, while supplies last. [ad_2] Source link

Outdoor 7.5ft Market Patio Umbrella for just $39.99 shipped (Reg. $60!) Read More »