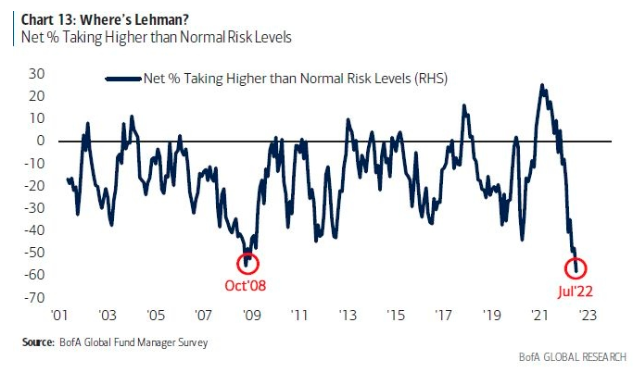

[ad_1] Kyle Prevost, editor of Million Dollar Journey and founder of the Canadian Financial Summit, shares financial headlines and offers context for Canadian investors. It was a big earnings week in the U.S. With so many unpredictable variables in the mix over the past three months, many investors were eager to see what was actually going on underneath the hood of some of the world’s largest companies. IBM (IBM/NYSE): Showing just how panicky the market is at the moment, IBM kicked off the earnings announcements this week with outperforming on both earnings and revenues, yet the stock price dropped 4% in extended trading on Monday. Earnings came in at $2.31 per share (versus $2.27 predicted) and revenues at $15.54 billion (versus $15.18 billion predicted). Free cash flow was down from past guidance, with IBM stating that suspending business in Russia was the main culprit. Johnson & Johnson (JNJ/NYSE): Johnson & Johnson continued the strong earnings news trend on Tuesday, announcing that even with strong U.S. dollar headwinds to battle, earnings were $2.59 per share (versus $2.54 predicted) and revenues were $24.02 billion (versus $23.77 billion). This good news was viewed with skepticism by the market as JNJ was down in early trading. Lockheed Martin (LMT/NYSE): Defense giant Lockheed Martin had a small earnings miss with an earnings per share figure of $6.32 (versus $6.39 predicted) and overall revenues coming in at $15.45 (versus $16.05 predicted). However, share prices traded up slightly on the news that the Pentagon was ordering nearly 400 more F-35 fighter jets. Tesla (TSLA/NASDAQ): Tesla reported a slight miss on revenues with $16.93 billion in total sales (versus $17.1 billion predicted), but it came out ahead on earnings per share numbers with an impressive $2.27 (versus $1.81 predicted). Interestingly though, Tesla decided to sell 75% of its bitcoin holdings during the quarter as well. Hmmm… Funny that one didn’t make it into CEO Elon Musk’s Twitter page. Tesla shares were up slightly in trading after the quarterly call. AT&T (T/NYSE): AT&T had perhaps the most noteworthy quarter of any company that has reported earnings so far. Its shares immediately dropped 9%+ on Thursday morning. Could bad news trigger such a rapid sell-off, you might ask? Well, the company added 813,000 monthly phone subscribers (substantially more than the 554,000 predicted by analysts), and adjusted earnings came in at $0.65 per share (versus $0.62 predicted). Revenues were almost identical to estimates, at $29.6 billion. Hidden from those raw numbers was the news that increasing numbers of customers weren’t paying their bills on time, and consequently, AT&T was forecasting $2 billion less in free cash flow for the year. With earnings results being quite variable so far this quarter, it’s somewhat difficult to come up with a one-size-fits-all theory. My major takeaway is that—despite continued solid earnings and sales numbers (for the most part)—investors are definitely looking at the glass as “half empty.” They are very worried about what lies ahead. Fund managers are now more pessimistic than they were at any point in the last 20+ years. Source: BofA Global Fund Manager Survey, as found on BNNBloomberg While trying to predict short-term market moves is a good way to make yourself look pretty silly, I can’t help but think there is a good argument to be made for a long-term contrarian play at the moment. The broader market trend was upward this week. But with investor sentiment still so low and valuation metrics such as price-to-earnings ratios continuing to fall, I think there will be some future investors thanking their present-day-selves for being greedy when everyone else was fearful in the summer of 2022. Want growth? Value? Who cares, as long as it makes money Contrary to the weird “good news triggers mediocre market response” stories above, Netflix (NFLX/NASDAQ) was up around 7% in early trading on Wednesday after revealing it lost a million subscribers in the last quarter. Sales revenue wasn’t quite as strong as predicted, coming in at $7.97 billion versus a predicted $8.035 billion. Many experts pointed to the following as causes for investors’ positive reactions: Earnings per share were up to $3.20 versus a predicted $2.94 Promises to charge more for password sharing should increase revenues The recently announced partnership with Microsoft to build an ad-supported platform option should also increase revenues Netflix led folks to believe subscriber numbers could be down by as many as two million—so losing “just” one million didn’t seem so bad! This could mark the beginning of investors looking at former “growth stocks,” like Meta (META/NASDAQ) and Netflix, as mature companies that need to be viewed as profit machines instead of as purely growth engines. All three MSOTM columnists (Dale Roberts, Jonathan Chevreau and myself included) have pointed out repeatedly that this is not the early 2000s when big tech names were “All sizzle and no steak.” Today’s tech companies might still exist online and have nerdy CEOs, but they are also highly profitable. Netflix and Meta (formerly Facebook) are so profitable, in fact, that given their recent share price meltdowns, they’re beginning to be added to “value stock” lists and indexes. What does this mean? They are generally trading at very low prices relative to their profits and free cash flow. For example, Meta’s free cash flow yield is above 8% right now! So even if you hate the idea of Metaverse and believe it’s just a giant black hole of money, the company is making more than enough profits to justify a substantial share price increase. Source: Seeking Alpha Similarly, Netflix could stall and grow at a much slower rate going forward. But as long as it can better monetize its customers (competitors like Hulu have proven ad-supported models can work) and keep their status as the preeminent streaming service (maybe easier said than done), then there may still be a bright future for this company. Mature companies tend to focus more on the “less sexy” topics of cost controls, upsells and maximizing customer value. While this