Hyliion Holdings Affiliate Files to Sell Nearly $18M in Stock

[ad_1] Hyliion Holdings Affiliate Files to Sell Nearly $18M in Stock [ad_2] Source link

Hyliion Holdings Affiliate Files to Sell Nearly $18M in Stock Read More »

[ad_1] Hyliion Holdings Affiliate Files to Sell Nearly $18M in Stock [ad_2] Source link

Hyliion Holdings Affiliate Files to Sell Nearly $18M in Stock Read More »

[ad_1] Xactus tapped Ross Gloudeman as the verification solutions provider’s general counsel and chief compliance officer. The executive will be responsible for strengthening Xactus’ regulatory compliance framework and administering regulatory changes required by the credit and mortgage industries, the firm said. Gloudeman started on Tuesday. Gloudeman’s career in mortgages and financial services will help “modernize compliance strategies for the quickly evolving mortgage landscape” as traditional approaches are falling behind, said Perry Steiner, chairman and CEO of Xactus said. Ross Gloudeman, general counsel and chief compliance officer of Xactus The executive was most recently the general counsel and chief compliance officer at Azminuth GRC, a regulatory tech company, for less than a year. His 15-plus years of career include three years at Home Point Financial, where he was promoted to senior managing director of enterprise risk and corporate governance and seven years at Black Knight Financial Services. where he left as chief compliance and regulatory counsel. Xactus, which says it has more than 6,500 clients including bank and nonbank mortgage originators, uses its proprietary technology platform to close loans quickly. Starting out with a combination of credit reporting companies CIS Credit Solutions and Avantus in 2020, the company moved into the appraisal technology business the following year and rebranded to Xactus in March 2022. Since then, the firm acquired MassiveCert, a software company that provides flood zone determinations for insurance, lending and real estate in July. With the acquisition, Xactus added flood services to its verification solutions “to address clients’ flood risk assessment needs,” the firm said. In June, the verifications solutions provider rolled out a monitoring program that scans residential addresses for changes in listing status. In a tight housing market, Xactus said it aims to help customers close loans more quickly. Amid the new acquisitions and program roll outs, Gloudeman said he hopes to contribute his compliance management approach to the firm. “We have a unique opportunity in a down market to help deliver the dream of homeownership by further enabling lenders’ decisioning and closing processes,” Gloudeman said. The post Verification provider Xactus hires chief compliance officer appeared first on HousingWire. [ad_2] Source link

Verification provider Xactus hires chief compliance officer Read More »

[ad_1] Calling all teachers! You can get a free coffee at Dunkin’ Donuts tomorrow! Tomorrow, September 1st, Dunkin’ Donuts is celebrating offering all teachers a free medium hot or iced coffee! No purchase necessary. Thanks, Hip2Save! [ad_2] Source link

Dunkin’ Donuts: Free Coffee for Teachers on September 1st! Read More »

[ad_1] Canada switches ministers in mini Cabinet reshuffle [ad_2] Source link

Canada switches ministers in mini Cabinet reshuffle Read More »

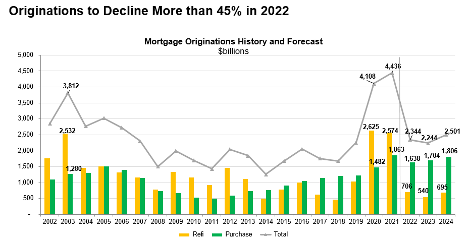

[ad_1] After two record-setting years of mortgage origination volume, the mortgage industry is contracting, sharply. Based on our read of 2021 Home Mortgage Disclosure Act (HMDA) data, we estimate that total originations volume last year was $4.4 trillion. By comparison, we are forecasting total volume of about $2.3 trillion this year, and similar levels over the next two years. One question that we receive all the time is, “How much overcapacity was there in the industry for this level of volume, and how much more do you think will be cut?” This is a complicated question, but our goal with this column is to provide our thoughts on how one might answer that question. Source: Mortgage Bankers Association Of course, the world will never stop providing positive and negative shocks. Think back to all that has happened over the last two and a half years. This estimate is only indicative of the path the industry is likely to take, absent a significant change in the level of volume over the next few years relative to our forecast. Ultimately, the best measure of whether the industry has too much or too little capacity for the volume being originated is profitability. When lenders are in the midst of a refinance wave, margins tend to widen as its all they can do to close the loans coming in the door. As some say during these refinance periods, “the fish are literally jumping into the boat.” On the other hand, when volume drops sharply as it has recently, pricing gets more aggressive, and fixed costs are spread over a smaller number of units, leading to tighter margins, or even losses. Source: MBA Quarterly Mortgage Bankers Performance Report: www.mba.org/performancereport According to MBA’s Quarterly Performance Report (QPR), net production income has averaged 54 basis points since 2008. This production margin reached a record 203 basis points in the third quarter of 2020, as lenders were swamped with refinance volume. In the past three quarters, it has dropped below this historical average. At 5 basis points in first-quarter 2022, and at a loss of 5 basis points in second-quarter 2022, the industry is now struggling with the perfect storm of lower volume, lower revenues, and higher costs per loan. The net loss at the industry level this past quarter matches the pattern we saw in 2018, with a run-up in rates and the end of a refi wave. Compared to 2018, the current cycle certainly has been more extreme in terms of the rapid spike in rates over a short period of time. So, one answer on how much capacity needs to come out of the industry is: “enough to experience gain in revenue or reduction in cost to bring margins back to their historical 54 bp average.” We will know that when we see it. But what our questioners are really asking is, “how fast we will get there?,” not just, “where we will end up?” If industry profitability is the result of having too much or too little capacity, how can we measure capacity directly? We need to examine both the number of employees and their productivity. During the latest refi boom, the hiring cycle was accentuated by constraints caused by the pandemic. Mortgage employee productivity went through the roof as overtime, retention bonuses, and signing bonuses were predominant methods for adjusting capacity. Now, lenders are in a position in which they must reduce their workforces, or risk a plummet in productivity or worse, profitability. Looking again at data from MBA’s Quarterly Performance Report, loans closed per production employee[1] per month (in the retail and consumer direct channels combined) ranged from 1.3 to 2.3 in the three years prior to the pandemic. That changed in 2020, with productivity peaking at 3.1 in the third quarter of 2020. Lenders talked about how difficult it was to hire experienced personnel during the early phase of the pandemic. Moreover, many lender executives worried that their teams were working too much with very heavy overtime costs. Given that the lockdowns prevented employees from doing much else, this high level of productivity was not going to be sustainable, even if mortgage demand continued at its record-breaking pace. Per the chart, productivity has since dropped rapidly back to more typical levels as the result of both employee fatigue and, more recently, lower mortgage demand. But this does raise the question – if lenders had so much difficulty hiring during the boom, does that mean there is less capacity to trim, with this year’s drop in volume? Perhaps so, but that may be difficult to see given the magnitude of the decline in volume. Source: MBA Quarterly Mortgage Bankers Performance Report: www.mba.org/performancereport Layoff announcements are in the news these days and some lenders have chosen to shut their doors. However, to the main question we had asked, how much reduction in employment are we likely to see? First, let’s examine various measures of industry employment. Perhaps the most used and frequently cited metric for mortgage industry employment is from the Current Employment Statistics (CES) program at the U.S. Bureau of Labor Statistics, which collects industry data on nonfarm employment, hours worked, and earnings of workers on payrolls during the data collection period. The monthly Employment Situation Summary news release based on the CES data is regarded as a key report in gauging the health of the overall job market. The monthly data on payroll counts are broken down by the type of establishment and the occupations within a particular industry. [2] For mortgage industry employment, the estimates are based on two main industry categories. The first category is real estate credit, which covers most establishments focused on lending with real estate as collateral. Examples of companies within this category include mortgage companies, reverse mortgage lenders, and home equity lenders. The second category is mortgage and non-mortgage brokers, which includes establishments that facilitate lending by bringing borrowers and lenders together. These broad categories include jobs that involve lending directly or supporting real

MBA economists: The overcapacity that still needs to be cut Read More »

[ad_1] This is a great deal on this Zollipops Clean Teeth Zaffi Taffy! Amazon has this Zollipops Clean Teeth Zaffi Taffy (10 oz) for just $6.62 shipped when you checkout through Subscribe & Save! Note: Once your order ships, you can go into your Amazon account and cancel your subscription if you don’t want recurring orders. Thanks, Hip2Save! [ad_2] Source link

Zollipops Clean Teeth Zaffi Taffy only $6.62 shipped! Read More »

[ad_1] Mourners mark Princess Diana's death in Paris, 25 years on [ad_2] Source link

Mourners mark Princess Diana's death in Paris, 25 years on Read More »

[ad_1] Craving ice cream? Stop by Walgreens to score Buy One, Get One Free Ice Cream! Through September 3rd, Walgreens is offering Buy One, Get One Free on select Ice Cream products! No promo code needed. [ad_2] Source link

Walgreens: Buy One, Get One Free Ice Cream Read More »

[ad_1] Toyota triples planned investment to $3.8 billion in U.S. battery plant [ad_2] Source link

Toyota triples planned investment to $3.8 billion in U.S. battery plant Read More »

[ad_1] This is a hot deal on these Seven7 Tummy-Control Jeans! Today only, Zulily has Seven7 Tummy-Control Jeans for just $19.99! Plus, when you shop through our link, you will save an extra 10% off making these only $17.99! Choose from lots of styles and colors. Shipping is free on orders over $89. And if you place one order today, the rest of your orders will ship for FREE through 11:59 p.m. PT tonight! [ad_2] Source link

Seven7 Jeans only $17.99 after Exclusive Discount (Reg. $79!) Read More »