India reports daily rise of 326,098 in coronavirus infections

[ad_1] India reports daily rise of 326,098 in coronavirus infections [ad_2] Source link

India reports daily rise of 326,098 in coronavirus infections Read More »

[ad_1] India reports daily rise of 326,098 in coronavirus infections [ad_2] Source link

India reports daily rise of 326,098 in coronavirus infections Read More »

[ad_1] While there were signs of a significant revival in the property market in the first quarter of 2021, a momentary halt in any upward trajectory is being seen now. [ad_2] Source link

Real Estate trends to watch out for during Covid-19 second wave Read More »

[ad_1] Secretary of Housing and Urban Development Marcia Fudge delivers remarks during a press briefing at the White House in Washington, U.S., March 18, 2021. REUTERS/Carlos Barria First, let’s set the record straight. Homeownership is critical to wealth creation, especially for establishing intergenerational wealth in America. When looking at net worth, even considering the fact that there can be periods of volatility, the ability for Americans to own a home has proven to be the best method for establishing a financial reserve for passing onto the next generation and to tap into for other financial needs. The debate that has occurred over the decades about renting vs. owning is answered with data. But it is true, not all should own or perhaps are able to own. But if you are able own a home, can qualify and commit to ownership, there is a strong argument to support doing so. One of the conundrums of homeownership is that it is limited to certain individuals meeting the necessary criteria. Unfortunately, in the U.S., these limits often reflect the ethnic divides that make up the nation. Today, white non-Hispanic homeownership rates are above 70%, while Hispanic and Black rates sit in the sub 50% levels. For Black homeownership in particular, there has been little improvement in the homeownership rate at all. I would argue that public policy has actually eroded the strength of forceful leadership needed to make any dent in this area. An effort to address this gap is once again being discussed by the new administration. President Biden, in fact, had a plank in his campaign calling for a $15,000 first-time homebuyer tax credit. The proposal has been met with resistance in a variety of policy arenas where the debate over the lack of single-family inventory for sale raises concerns that a tax credit would simply exacerbate the already challenging environment that some argue is artificially inflating home values. The rest of this content is for HW+ members. Join today with an HW+ Membership! Already a member? log in HW+ includes weekly long-form digital content, HousingWire Magazine, access to HousingStack, and free admission to all HousingWire virtual events. The post How do we make real progress on the homeownership gap? appeared first on HousingWire. [ad_2] Source link

How do we make real progress on the homeownership gap? Read More »

[ad_1] The post The Cashflow Quadrant: The Path to Financial Freedom appeared first on Millennial Money. Meet Phil. Phil is pushing 40 and entirely dependent on his full-time accounting job for survival. He works for someone else, making their company money all day with his hard work, and consistently goes above and beyond for the organization. Then there’s Amber. Amber is the same age as Phil, and they’re both middle class. But she has three sources of income, including two growing side hustles that could quickly turn into bona fide small businesses in the near future. Right now, Amber is already making more money than Phil. And soon, thanks to her hard work, she’ll be in a position to let her side hustles start earning her a solid full-time income. For many reasons, Amber is in a much stronger position than Phil, who better get his act together if he hopes to retire within the next 30 years. What’s interesting is that most workers learn Phil’s approach to personal finance, going to school for four years, getting a job, and spending 40 years in the workforce working for other people’s companies. Most people think Phil’s way is the safe way. Yet the traditional work model no longer provides as much stability as it once did, and it’s outdated. The world has changed drastically over the last decade, and the workforce is still catching up to the idea that it’s better to forge your own path and rely on yourself for making money. It’s time to reignite your career and realize your true potential. Unfortunately, this won’t happen overnight; you’ll need to take baby steps to make it happen. But one thing that may help you get there is the cashflow quadrant. Let’s take a closer look at this revolutionary idea. What is the cashflow quadrant? The cashflow quadrant is a chart that describes the four main options for making money. The concept is the brainchild of author Robert Kiyosaki, who created the bestselling Rich Dad, Poor Dad series of books that are filled with financial advice. Kiyosaki’s book “Cashflow Quadrant” outlines why some people work less and earn more and, by doing so, are able to attain financial freedom. Kiyosaki asserts there are four main areas of the quadrant you can fall into. The left side: Active income The left side of the quadrants is active income. In other words, you have to consistently work to cover your basic living expenses. As Kiyosaki points out, the left side pays the highest tax rates and trades their time for money. Employee Employees work for companies and exchange their time and skills for a paycheck. The only way employees make money is through active work. Making more money typically involves switching jobs or getting a raise or promotion. Self-employed Self-employed individuals are business owners. However, your business actually owns you because you’re still working and therefore trading time for money. Think about a dentist with her own practice. Somebody’s got to clean teeth and fill cavities! So, in a sense, even if you own a business, you’re still employed. If you stop working, the business stops making money. The right side: Passive income The right side of the quadrant deals with passive income. On this side of the quadrant, your money works for you. This side, Kiyosaki says in the Rich Dad’s guide, pays the least in taxes, maximizes the tax code, and creates assets that produce a continuous cash flow. Business owner Business owners create a system that generates money and hire people to work for them. As the owner of your own business, you don’t have to be actively involved in the day-to-day operations to make money. The business does this for you; think about how rich Microsoft made Bill Gates. There are many ways to excel at entrepreneurship. And the truth is it’s easier than ever today to launch a business and achieve financial success. You could launch a business through Amazon, start a dog-walking business, or even sell graphic design work or photos online and collect royalties as an art entrepreneur. In the digital age, starting a business doesn’t have to be a massive ordeal. Investor The lower right portion of the cashflow quadrant is for investors. In this section, your investments generate recurring payments for you through vehicles like the stock market and real estate. You don’t have to work or manage anything in this group unless you want to because your money does all the work for you. Learn more: 16 Best Passive Income Apps To Make Money Best Online Business Ideas for 2021 The Pros and Cons of Investing in Real Estate How to use the Rich Dad’s cashflow quadrant 1. Determine where you fall in the cashflow quadrant This is the easy part. Identify your position in the quadrant. You’re either an employee, self-employed, a business owner, or an investor. No matter where you wind up, understand that this situation is temporary. If you’re an employee, you can become self-employed. If you’re self-employed, you can become a business owner. And if you’re a business owner, you can become a full-time investor. At the same time, it goes in both directions. Full-time investors who don’t manage their money properly or run into a patch of bad luck can easily wind up having to go back and start from scratch again with a full-time job. 2. Assess your situation Spend time thinking about your situation and how you got there. You should also think about why you’re still there and not in a more lucrative role. Challenge your way of thinking and assess whether you could improve your situation by making some small changes. For example, some employees may like their job and don’t care to climb any higher because of a sense of security and a nice income. However, it’s worth considering just how secure a full-time job really is. If you’re at the mercy of a boss or a big business, your role

The Cashflow Quadrant: The Path to Financial Freedom Read More »

[ad_1] Don’t miss this rare sale on Millie Loves Lily Swimwear! Through the end of today, Zulily is running a sale on Millie Loves Lily Kids’ Swimwear and you can get up to 50% off regular prices! There are SO many cute suits to choose from, including animals, floral, patterned, bright colors, themed, and more! They sent us a few swimsuits for Kierstyn to try, and I’m so excited about them! I love the bright colors and fun patterns. And they have a UV protection rating of UPF 50+, which is really nice. Plus, today only, our readers can score FREE shipping on orders over $45! Otherwise, shipping starts at $5.99. AND if you place one order today, the rest of your orders will ship for FREE through 11:59 p.m. PT tonight. Go here to shop this swimsuit sale. [ad_2] Source link

I’m so excited about these cute swimsuits for Kierstyn!! (Up to 50% Off!) Read More »

[ad_1] Death toll rises as violence rocks Gaza, Israel and West Bank [ad_2] Source link

Death toll rises as violence rocks Gaza, Israel and West Bank Read More »

[ad_1] International orders at Rs 18,439 crore made up 36% of the total order inflow, with receipt of biggest Solar PV plant order and transmission line orders. [ad_2] Source link

Q4 earnings: L&T net rises 3% to Rs 3,293 crore; fresh orders stay under pressure Read More »

[ad_1] Credit can be confusing, but it can also be a huge asset going into the home-buying process. A good credit score increases the likelihood of qualifying for a mortgage because it indicates to the lender that you’re more likely to make timely payments on your loan. Even better, a solid credit score gives you, the potential borrower, a better chance at a lower interest rate. This might result in thousands of dollars saved over the life of the loan. But if you’re finding that your credit score is more of a hindrance than an asset to your home-buying endeavors, or are unsure where you stand with your credit health, never fear. There are methods to improve and maintain your credit as you move toward buying a home. Make Timely Payments You can’t obtain a good credit score without first establishing credit. This can be done by obtaining a loan or line of credit, like a credit card. If you’re looking to improve your credit score, start by demonstrating you manage your credit wisely. Use it to make responsible purchases, and pay the bills on time, every time. If you have a history of late payments, try to make timely payments going forward. Checking your credit report can help you keep track of any late payments. There are many tools online that will allow you to view your credit report once per year, without impacting your credit score. Take advantage of these tools and make sure all of your debt payments are reported accurately. . Should you find a payment was incorrectly reported as late, you can dispute it with the credit bureau that reported the timing of the payment. You can also dispute it directly with the creditor that initially sent the information to the bureau, following the instructions provided by your lender for filing the dispute. Take into account that if you dispute information on your credit report, the credit reporting agency or the lender typically has 30 days to investigate the claim and may request additional information from you to support your claim. Strategically Diversify Your Credit Opening a new account may help build your credit. Consider a new credit card, or taking on installment debt – a loan that is repaid by the borrower in regular installments. This is commonly referred to as “credit mix” and demonstrates your ability to manage multiple types of loans. If you use your credit mix prudently, it may contribute to boosting your credit score. That said, be wary of opening new lines of credit if you are nearing or already in the home-buying process. “If you are in the process of buying a home, then that should be your one and only credit acquisition activity,” said John Ulzheimer, a former credit bureau insider and author whose books on the subject of credit include The Smart Consumer’s Guide to Good Credit. By taking on large amounts of debt just before they apply for a mortgage loan, Ulzheimer said, a home loan applicant may affect how a lender evaluates their application. If you’re in the process of being evaluated for a home loan, it’s also not the time to disrupt your credit picture by making a major purchase using credit. Incurring new debt could impact the likelihood of approval. Don’t Shut it Down Don’t close out your credit sources – such as canceling a credit card – just to prove you don’t need them. This may lower your overall available credit. It may be more favorable to your credit profile to keep those accounts open and unused or lightly used if you are making payments timely. “You’re better off using that credit card for a small payment at the grocery store, and then paying it off at the end of the month,” said Citi Area Lending Manager Marc Souza. You could also use that card to cover any small subscriptions services. Just be sure that the balance on the card is set to automatically be paid monthly. This will maintain your available credit amount and reduce the risk of an account being closed due to inactivity. Look at your Student Loans While student loans can affect your credit, it’s not always in a negative manner. Demonstrating that you can pay a specified amount over a period shows a solid track record. If you have questions about your loans, don’t hesitate to consult an expert. Whether contemplating a consolidation of student debts or forbearance forgiveness, be sure to have those discussions with a credit expert prior to making any moves. Creditors can help you form the best strategy on dealing with loans. Since some loan programs analyze student debt differently than a credit card or car loan, experts will aid you in setting priorities to improve your credit. Keep in mind other key elements besides your credit score When a lender is preparing to loan you money for a mortgage, your credit score is a measure of reliability. The higher the score, the more trustworthy you appear. Plus, a higher score may qualify you for lower mortgage rates. But while your score is a vital component, it’s not the only one. Lenders will also look at your income, employment history and capacity to take on the new payment. The Loan to Value ratio, where lenders look at the appraised value of the home in comparison to the loan amount, is also important. Improve your DTI Ratio Your debt-to-income ratio, or the amount of your gross monthly income that goes toward your monthly debt, influences your ability to get a mortgage. In the eyes of a lender, the lower the DTI, the more likely you can pay. If you incur new expenses during the evaluation period, that will be calculated into your DTI. To lower your DTI, attempt to pay off other loans or lines of credit in full. Making monthly payments toward your debt will not lower your DTI – only eliminating entire balances will. One strategy to employ is entirely paying

Why does credit matter so much in the home-buying process? Here’s the scoop Read More »

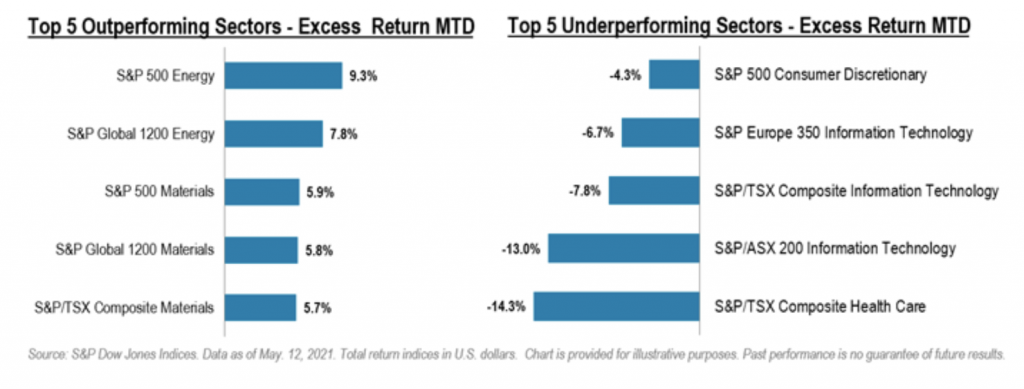

[ad_1] Each week, Cut the Crap Investing founder Dale Roberts shares financial headlines and offers context for Canadian investors. The Nasdaq is having a bad day…and month Wow, what a week. Stocks are taking it on the chin in Canada, the United States and around the globe. And U.S. tech stocks that led positive gains in 2020 are getting hit harder than the broad market. The tech-heavy Nasdaq 100 (QQQ) is down 7% over the last month, while the S&P 500 (IVV) is down 1.5%. The Nasdaq is below where it was on January 8, 2021. The tech-heavy, and certainly still growth-heavy Nasdaq is having trouble finding another gear, falling 2.6% on Tuesday, May 11, its worst day since March. Nasdaq can’t break out of the gravity of 2021—and that gravity is the force of inflation fears and the fear of rising rates. Investors, when they factor in inflation fears, will move away from tech stocks because they think of tech stocks as longer-duration assets which will not pay until well into the future. On Tuesday of this week, the U.S. released inflation (CPI) data that surprised with its upside implications: Meaningful inflation is being created in the very early stages of the economic reboot. Data from the U.S. Bureau of Labor Statistics yesterday showed that inflation this year, from January to April, climbed at its fastest pace since 2008. The Consumer Price Index came in at 4.2% vs. expectations of 3.6%, which is already ahead of the Fed’s 2% target. This from S&P Global, sent to my email inbox… “According to economists, rising unemployment and high inflation (‘stagflation’) may be the result if the money supply is pumped too hard and fast by the authorities, especially if there is also a supply shock—a spike in the oil price, for example. The current massive U.S. fiscal and monetary stimulus, combined with soaring raw material prices, last Friday’s employment report shocker and yesterday’s eye-watering inflation print—MoM growth was the highest since 1982—have spooked the markets.” BMO says inflation is more than just the base-year effects (we are starting from some pandemic-induced low prices from a year ago), and meaningful inflation appears more prevalent across a few recent timelines as well. Three-month inflation is at 5.6% annualized, and the 6-month rate is at 3.3% annualized. Thanks to Scott Barlow of the Globe and Mail for this tweet and numbers: BMO: "U.S. Inflation: It’s Not Just Base Effects" pic.twitter.com/VyTCtVYzmv — Scott Barlow (@SBarlow_ROB) May 13, 2021 And with the increase in inflation, your U.S. stocks won’t be making you any real return (inflation-adjusted), according to Liz Ann Sonders, the chief investment strategist at Charles Schwab. The real earnings yield has turned negative, and the real earnings yield for S&P 500 is at its lowest since 1981. S&P 500 real (inflation-adjusted) earnings yield has now fallen sharply into negative territory & is at its lowest since 1981 pic.twitter.com/OGv5risjdv — Liz Ann Sonders (@LizAnnSonders) May 13, 2021 Perhaps that lack of real earnings is and will weigh on stock prices. As investors, we want to own real earnings, in tandem with earnings growth and revenue growth. A real U.S. stock market correction, including growth-heavy tech and the broad markets, would be a healthy event. That would allow investors in the accumulation stage to load up at lower price, and potentially with great current earnings. For those of us in the retirement, semi-retirement or near-retirement stage, those corrections are not useful if we’ve planned on selling shares (near-term) to create income. Once again, accumulators might root for a real U.S. stock market correction, and a return to real earnings. Lower prices are good. We’ll see if the markets can blow off the inflation scare from this week. And, that said, on Thursday, May 13, U.S. stocks were back in positive territory. In early Friday trading US stocks were adding on more gains. The next few weeks might send some strong signals. Does this correction have legs? Rising rates do not always accompany inflation This big and very interesting question was put forth by Mark Noble of Horizons ETFs: Do rising rates always accompany inflation? I would guess mostly yes. I would be mostly wrong. I suggested to Mark that we check in with Mike Philbrick of ReSolve Asset Management—and, right on cue, Philbrick jumped in with the answer and charts. yes – we faced this through the 1930s to the 1950s. This is where the term of transient inflation is stemming from.You can observe several periods where inflation spikes and interest rates do not – PLUNGING the real rate of return (blue line) negative.https://t.co/MtnyVkVsv3 pic.twitter.com/6SlMAv3WeG — Mike Philbrick (@MikePhilbrick99) May 5, 2021 You can go to that live link on Longtermtrends to see a description of the chart, and the interpretation of real interest rates. Real interest rate is the rate of return that also factors in the inflation at the time. I’ll admit I would have guessed that a serious increase in inflation would be accompanied by short-term rising rates, at least. Central banks increase rates to keep a lid on growth and inflation. But that was not the case in the post-WWII recovery. I asked Phibrick for clarification on why rates stayed low in that period. He offered… “The bottom line is the central banks control interest rates and when they cannot afford to pay any higher amount of debt due to the [size] of the debt, they pin rates low. This is YCC, or Yield Curve Control being talked about. Post-Second World War, the situation on debt was similar—for example debt, was large and so rates were kept artificially low.” Yes, we are in that same situation today; with their massive borrowing and printing of money, governments (and the world) cannot afford higher rates or higher borrowing costs. Philbrick added… “Also in WWII, there were many price controls put in place and as those price controls were removed, you saw sudden spikes in inflation in certain areas but rates were kept

Making sense of the markets this week: May 17, 2021 Read More »

[ad_1] The post 3 Growth Stocks Off 25% with Massive Upside Potential appeared first on Millennial Money. 2020 was crazy, right? Last March, when faced with the greatest economic decline since the Great Depression and a stock market that had its fastest 30% sell-off ever, the federal government forcefully stepped in and provided support to prevent the economy from crashing. While the verdict is still out for the economic recovery, the stock market was certainly saved. Last year the S&P 500 climbed 16% higher for full-year returns but nearly doubled from the lows established in March. In fact, large cap growth stocks like Apple, Amazon, and Tesla gained 82%, 76%, and 695%, respectively last year alone! It wasn’t just Wall Street that saw account balances swell. Instead, an unlikely group that benefited the most might be young retail investors who live by the phrase “you only live once,” or YOLO. The so-called “dumb money” stepped in to snap up shares of growth stocks and cryptocurrency on the cheap with a few becoming millionaires in the process. The economy appears to be slowly healing as more needles find their way into arms and the pandemic’s end seems in sight. So naturally, you’d expect these growth stocks to continue rocketing higher… and you’d be mostly wrong. In fact, this is the first year since 2016 that growth stocks are underperforming compared to value stocks. 2020’s stock market titans are 2021’s laggards This year has seen an amazing reversal with high-growth stocks being sold off in a rout. For an example of just how swift the change in fortunes has been, look no further than two of 2020’s biggest winning growth investors: Cathie Wood and Chamath Palihapitiya. Wood’s ARK actively managed ETFs exploded last year, catapulting her to first-tier investment manager status despite only founding the company six years prior. Palihapitiya led the SPAC revolution with his Social Capital Hedosophia blank check companies and became known as “the SPAC king,” a legend among Reddit investors and Twitter. This year has been more difficult for both. Cathie Wood’s ETFs are down in 2021 with the flagship ARKK ETF down 18% year to date. That said, she’s significantly outperforming Palihapitiya’s SPACs Virgin Galactic (-32%), Clover Health (-51%), and Opendoor (-37%) SPAC reverse mergers. The situation looks significantly worse when you use drops from recent highs–Virgin Galactic is down more than 70% since February! While they’re noteworthy, they’re certainly not alone. Growth stocks are getting pummeled this year with many down 50% or more from highs established in February. Why investors should be happy about growth’s sell-off At Millennial Money, a common question we hear is “what’s going on with the market?”We often find our answers shock people. Instead of being nervous or concerned about the recent growth-stock sell-off, we’re elated to buy stocks on sale! That’s because we know two things: first, we share legendary investor Robert Arnott’s viewpoint that “in investing, what is comfortable is rarely profitable,” as well as understanding that to generate above-average returns, you must control your emotions better than the average investor. Second, we know that we’re going to be net buyers of stocks over the next 10 years and we like to pay less for growth. That’s why we feel that for long-term investors, many growth stocks have been unfairly sold off and present opportunities to buy at a discount. We had our team of investors pick out three high-quality stocks that have seen recent sell-offs. Each stock is riding trends that could last a decade or more and is a leader in their industry. If you’re looking to find opportunities that could look like fantastic buys at today’s prices five years from now, you’ll want to add these stocks to your watchlist today! Pick Like A Pro Where to invest $500 right now Are you ready for “maximum upside?” Motley Fool Rule Breakers is led by legendary investor David Gardner and pinpointed Tesla at $6.29, Salesforce at $6.89, and Shopify at $21.02. (It trades for more than $1,000 per share today!) Here’s why you’ll want to get the full details on Rule Breakers today. The service just announced its top 10 “best buys now” across the entire stock market. Whether you’re starting with $100, $500, or more, you’ll want to get the full details! Click here to learn more Upstart is one of the market’s most compelling growth stories Upstart (Nasdaq: UPST)Current Price: $84.051-Year Price Target: $131.17Implied Upside: 56.1% Eric Bleeker (UPST): On March 5th, Millennial Money featured Upstart as our Stock of the Week. Less than two weeks later, the company released its fourth quarter earnings and there was a bombshell inside. Upstart, which grew revenue 42% in 2020, issued guidance that revenue growth would accelerate to 114% in 2021 and reach an expected $500 million. That kind of business acceleration from a disruptive company is what growth investors dream of, so it wasn’t surprising that Upstart stock jumped from $60.79 the day before it announced earnings to a high of $165.66 three days later. What was more shocking was that Upstart’s stock rapidly retreated in the weeks that followed. Fast forward to this week and the company just issued its first quarter earnings and once again increased guidance for 2021. The company now expects revenue to grow 157% this year. In pre-market trading the day after announcing its latest earnings, Upstart was up 27%. However, with a sell-off happening across growth stocks, Upstart saw its 27% pre-market gains whittle down to 2.6% by the end of the day. I don’t know how to be more clear that seeing a stock accelerate from 42% sales growth one year to 157% the next is rare. That kind of inflection point almost never happens. Yet, Upstart is trading at a lower price today than it was three months ago. To me, this is the quintessential example of buying great companies when there’s “blood on the streets.” Wild price increases in Reddit stocks and special acquisition companies (SPACs) spoke

3 Growth Stocks Off 25% with Massive Upside Potential Read More »