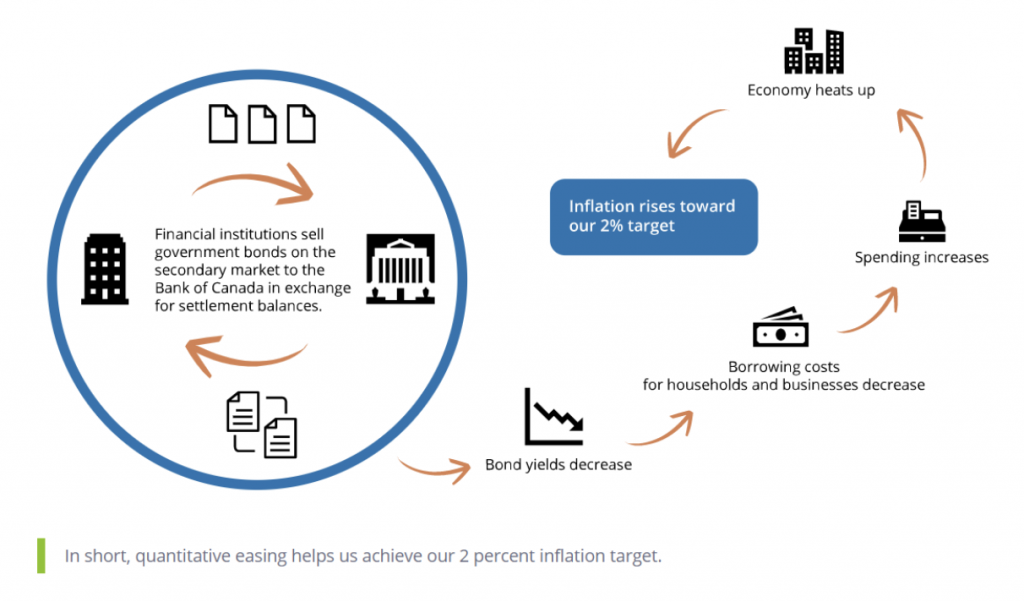

[ad_1] Each week, Cut the Crap Investing founder Dale Roberts shares financial headlines and offers context for Canadian investors. Are the markets throwing a taper tantrum? The term “taper” and the possibility of a “taper tantrum” jumped into business news and headlines this past week. What is all of this taper talk? And what does it mean for our stocks and bonds, and other investments? Here’s the background. To help keep rates low, central banks buy their own government bonds. That link to the Bank of Canada site explains the bond-buying process (termed QE, or quantitative easing). And here’s the rationale from that BOC page… “QE sends a signal that we intend to keep our policy interest rate low for a long time—as long as inflation stays under control. By giving more certainty that our policy interest rate will remain low, QE can help reduce longer-term borrowing costs for businesses and households.” And in chart form… Source: Bank of Canada Central banks are working to stimulate growth as part of their goal to achieve a 2% inflation target. Other government forces are involved as well; in what is called “fiscal policy,” some programs send monies directly to citizens to stimulate spending and growth. A recent example of fiscal policy is the CERB program that cut cheques to Canadians out of work due to the pandemic. We also saw government payouts and loans for Canadian businesses. The central bank will factor in all of the stimulus as they keep an eye on the economy and the consumer. When they’ve achieved their growth and inflation targets, they can ease off on those bond-buying programs; that is, they will taper their bond-buying. And when we experience tapering or hear talk of tapering, the markets may not like it. They might get a little skittish. Heck, they might even throw a taper “tantrum.” From that Investopedia link… “As a result of their dependence on sustained monetary stimulus under QE, the financial markets may experience a downturn in response to tapering; this is known as a ‘taper tantrum’.” And, right now, a taper tantrum is the talk of the town (OK, the talk of Wall Street and Bay Street) as market watchers wonder how investors will react. Also at play is the level of rate increases introduced by these central bankers. In last week’s post, we looked at some Canadian inflation stats and pondered whether U.S. Federal Reserve Chair Jerome Powell might start to increase rates sooner than expected. In 2013, we experienced the original taper tantrum. Bond yields spiked considerably at the mere mention of tapering. As always, that spike will sent the value of the bond plummeting. The stock markets took a bit of a spill as well, but recovered as the Fed backed off of its threat to taper, and went back to more bond buying (QE). Here’s some recent Fed speak, as reported on Seeking Alpha. They are being very cautious in tone, suggesting the U.S. Federal Reserve will not hike rates prematurely. Powell continues with the suggestion that inflation is transitory and manageable. But the markets on both sides of the border are addicted to the various forms of stimulus. What happens when the central banks even suggest that they’ll take away the punch bowl? It’s a tricky dance. This week, U.S., Canadian and international stock markets are answering the Fed speak with market highs, or near-highs. On my site last week, I attempted to interpret what the bond markets are trying to say; it sounds like they are perhaps not buying the long-term growth story. They might be saying after the initial inflation burst, we’re back to disinflation, or perhaps even deflation is a possibility. The stock and bond markets are talking. Are they on the same page? What the heck is going on with bitcoin? Readers of this column know that I am a fan of investing in bitcoin. While I’m curious about other cryptocurrencies and their various value propositions, I am currently invested only in bitcoin. I see it as digital gold. I am also invested in “real” gold and other commodities or commodity-related stocks. Over the last year, bitcoin is up by more than 250%. However, year-to-date, it’s up “only” 16%. Of course, this could all change in a hurry by the time you read post—with prices changing in either direction. As I’ve often mentioned (the obvious), bitcoin is an incredibly volatile asset. While it can be explosive to the upside, it can fall in quick order as well. On the Moolala podcast in May, I suggested to the wonderful and always entertaining host, Bruce Sellery, that bitcoin investors should certainly be prepared for massive corrections—even the frightening 80% variety that we’ve seen in the past. In that podcast I also offered that bitcoin is “just another asset” for me. I will hold and rebalance. Well, be careful what you ask for. From the highs of April, the price of bitcoin has been cut in half. This week it’s in the $32,000US to $35,000US range. So, what happened? Elon Musk (CEO of electric vehicle-maker Tesla) originally gave bitcoin a boost by accepting bitcoin as payment for vehicles. He then reversed his call on that payment option due to the environmental concerns of bitcoin mining. As a result, the price took a major hit that began a quick and continued decline. Chinese governments also piled on, banning bitcoin mining in many regions. But bitcoin is fighting back. In this “Making sense of the markets” post, we looked at the bitcoin energy council and how the bitcoin community would help bitcoin “go green.” They want to manage the PR problem for bitcoin as well. And as Greg Foss of Validus Power Corp offered in that MoneySense link, many of these miners are packing up and heading to greener pastures, such as Canada. Can green up its production and image? This Seeking Alpha post, ”Bitcoin goes green in major reversal,” laid out the potential for a positive being